Angelo Silva

Apr 12, 2019

4 mins

Yield Curve Inversion

Outlook. The local yield curve remained slightly inverted at the 1-yr against the 10-yr as the government borrowed at even higher rates than secondary market rates. The rate downtrend to 5.6% proved shortlived and unsustainable as the rally was sold down on the view it won’t take long for government’s strong cash needs to resurface despite an earlier announcement that second quarter borrowing will be lower than the first quarter of this year by Php45bn to Php315B. This is also lower than Q2-2018’s P325B borrowing program. As rates go higher, we see accumulation to position for the widely expected RRR cut in May when the monetary board is scheduled to meet again and inflation is expected to trend even lower. Bangko Sentral (BSP) officials indicated its first clear signal last week that a cut in policy rates and reserve requirement will only be considered if inflation eases further down to below 3%, which opened a window for profit taking last week and pushed yields up.

Local inflation fell to 3.3% in March, lower than February’s 3.8% and consensus estimate of 3.4%. This was also within the BSP’s expected range of 3.1%-3.9% and brought year-to-date inflation down to 3.8%. Growth of rice prices decelerated year-on-year (1.4%) and dipped month-on-month (-0.7%) with the onset of summer harvest season and arrival of imports. Core inflation eased to 3.5% from 3.9% in the month prior. Conflict in Libya presents upside pressure on oil prices but will be offset by the signing of the IRR of the rice tarrification law. Trade balance will be reported this Thursday.Market review. The local benchmark yield curve rose by 8bps on average week-on-week (WoW) during a profit-taking week. The spread between the local 10-yr local benchmark and the 10-yr US Treasury (UST) widened to 337bps from 320bps in the week prior as the former rose to 5.87%, 27bps higher WoW, while the latter likewise rose by 9bps to 2.50%. Year-to-date, the local yield curve was down by an average of 104bps while the 10-yr was down by 120bps. Yields of ROPs were up by 5bps on average, tracking US Treasuries which also increased by 6bps on average.

Average total daily volume down 56% week-on-week (WoW) to Php15.7bn. The liquid yield curve rose an average of 9bps WoW as the front-end (364-day T-bill) dipped by 2bps to 6.08%, the belly (FXTN 10-63: 9.5yrs) rose by 26bps 5.87%, while the tail (R25-01: 20.5yr) was up by 14bps to 5.96%. Traders were defensive ahead of the inflation report. Secondary trading average volume fell by 56% to Php15.7bn as both T-bond and T-bill trading volume fell by more than half to Php13.6bn and Php2.1bn, respectively. The Bureau of the Treasury’s (BTr) fully awarded its Php20bn auction of re-issued 10-yr T-bonds. The auction fetched an average rate of 5.954%, slightly higher than the prevailing secondary market rate of 5.87% but within the expected rate of 5.8%-6.0% of the market. The auction was 2.3x oversubscribed. Lastly, the latest Php20bn T-bill auction was only partially awarded at average rates of 5.612%, 5.982%, and 6.052%, respectively, -3bps, +3bps, and +4bps lower/higher than the previous auction and was 1.3x oversubscribed. Only the 91-day was fully awarded.

Emerging Markets’ (EM) 10-year flat, up by 1bp (WoW). Yields of EM bonds we follow were flat, up by just 1bp on average as concerns about Libya and its oil supply pushed oil prices up. Turkey (10-year yield -59bps), South Africa (-10bps), and Brazil (-8bps) outperformed last week, while Argentina (10-year yield +169bps), the Philippines (+26bps), and Israel (+19bps) underperformed.

USTs up 6bps WoW. US Treasuries were up by 6bps WoW on average as the 10-yr UST likewise rose by 9bps to 2.50%, fuelled by US-China trade deal optimism and positive economic data released during the week. There were 196,000 new jobs in March from February’s upwardly revised 33,000 (from 20,000) and beat expectations of 170,000. Hourly wages grew by 3.2%, down slightly from 3.4% in February. Trump also announced that an “epic” deal might be coming within the next few weeks. Last week’s rise helped return the yield curve to an upward slope last week after inverting the two weeks prior, a cause for concern for some investors that took it as a recession signal.

Read full article here.

Related Articles

Insights and Announcements

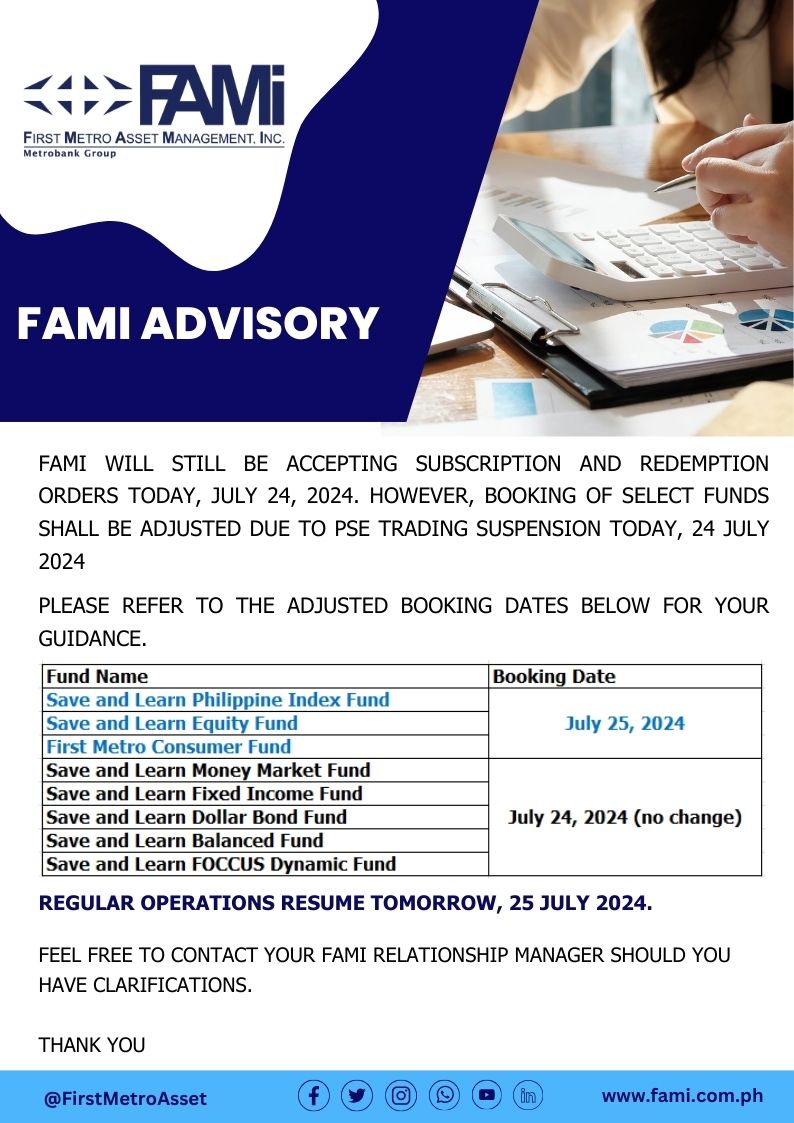

FAMI BOOKING ADVISORY