Angelo Silva

Oct 09, 2018

4 mins

Rising Bond Yields

Outlook. September inflation came in at 6.7%, below the BSP and consensus estimate of 6.8% but still within the forecast range of 6.3%-7.1%. This brought year-to-date headline inflation to 5.0%, still below the BSP’s forecast of 5.2% for the year but outside its target range of 2%-4%. Inflation was expected to have peaked in September but may remain elevated in the last quarter of the year, a seasonally-high inflation period. Bond yields may remain elevated as investors remain cautious of inflation. Positive developments in US trade relations with Mexico and Canada and robust economic data add upward pressure on local bond yields. The US 10-yr Treasury bond jumped from 3.06% at the start of last week to an intraday high of 3.25%, the highest since 2011, sparked by positive developments in trade policies and optimistic comments by Fed officials. One more Fed hike is expected in December and another four in 2019, which may necessitate more hikes by the Bangko Sentral ng Pilipinas (BSP).

Market review. The local benchmark yield curve rose by 27bps on average week-on-week (WoW) as the market remained cautious of breakaway inflation. The spread between the local 10-yr local benchmark and the 10-yr US Treasury (UST) widened to 457bps from 418bps in the prior week as the former rose by 57bps to 7.80% (bid; latest interpolated rate at 7.50%) while the latter was up by 18bps WoW to 3.23%. Yields of ROPs rose by 22bps on average, tracking the movement of the UST curve which likewise rose by 11bps on average.

Average total daily traded down 4% week-on-week (WoW) to Php4.3bn. The liquid yield curve rose by an average of 14bps WoW as the front-end (364-day T-bill) rose by 42bps to 5.69%, the belly (FXTN 10-63: 9.5yrs) up by 52bps to 7.75%, while the tail (R25-01: 20.5yr) shed 17bps to 7.83%. Secondary trading average volume fell by 4% to Php4.3bn, still thin, as T-bond volume recovered by 53% to Php2.7bn. On the other hand, T-bill volume shed 41% to Php1.6bn. The latest Php15bn auction of 91-day, 182-day, and 364-day T-bills was partially awarded with accepted bids for the 91-day, 182-day, and 364-day bids averaging at 4.404%, 5.684%, and 5.883%. Only the 91-day and 364-day T-bills were fully awarded. Lastly, the Php15bn offering of 5-yr T-bond was also just partially awarded at an average rate of 7.342%. Demand for the paper was tepid at just 1.1x bid-to-cover.

Emerging Markets’ (EM) 10-year up 19bps (WoW). Yields of EM bonds we follow were up by 19bps WoW as US rates ended the week sharply higher. Brazil (10-year yield -42bps), Czech Republic (-4bps), and Chile (flat) outperformed last week, while Turkey (10-year yield +246bps), Philippines (+57bps), and Indonesia (+26bps) underperformed.

USTs up 11bps WoW. US Treasuries were up by 11bps WoW on average as the 10-yr UST spiked by 18bps to 3.23%, fueled by Fed Chair Powell’s comment that the US economy was firing on all cylinders. Data on September’s ISM non-manufacturing index released last week showed its highest expansion of 61.6 since it was created last 2008. The figure outperformed expectations of 58 for the month and 58.5 in August. The manufacturing index in the same period also showed a still-high 59.8 expansion from 61.3 in August, the highest in a decade. Meanwhile, hiring eased to 134,000 for September while unemployment fell to a new low of 3.7%, down from 3.9% in August. Growth in hourly wages cooled to 2.8% form 2.9% in the month prior. The figures suggest that the labor market remains tight, with hiring outpacing labor-force growth and nearing full employment, though it’s yet to spill over to hourly wages. In the trade policy front, Canada just joined the US and Mexico in a revised NAFTA deal which is now called the United States-Mexico-Canada Agreement, or USMCA. The market cheered for the development, but China still looms in the background. December hike odds rose from 77% to 84% by the end of the week.

Read full article here.

Related Articles

Insights and Announcements

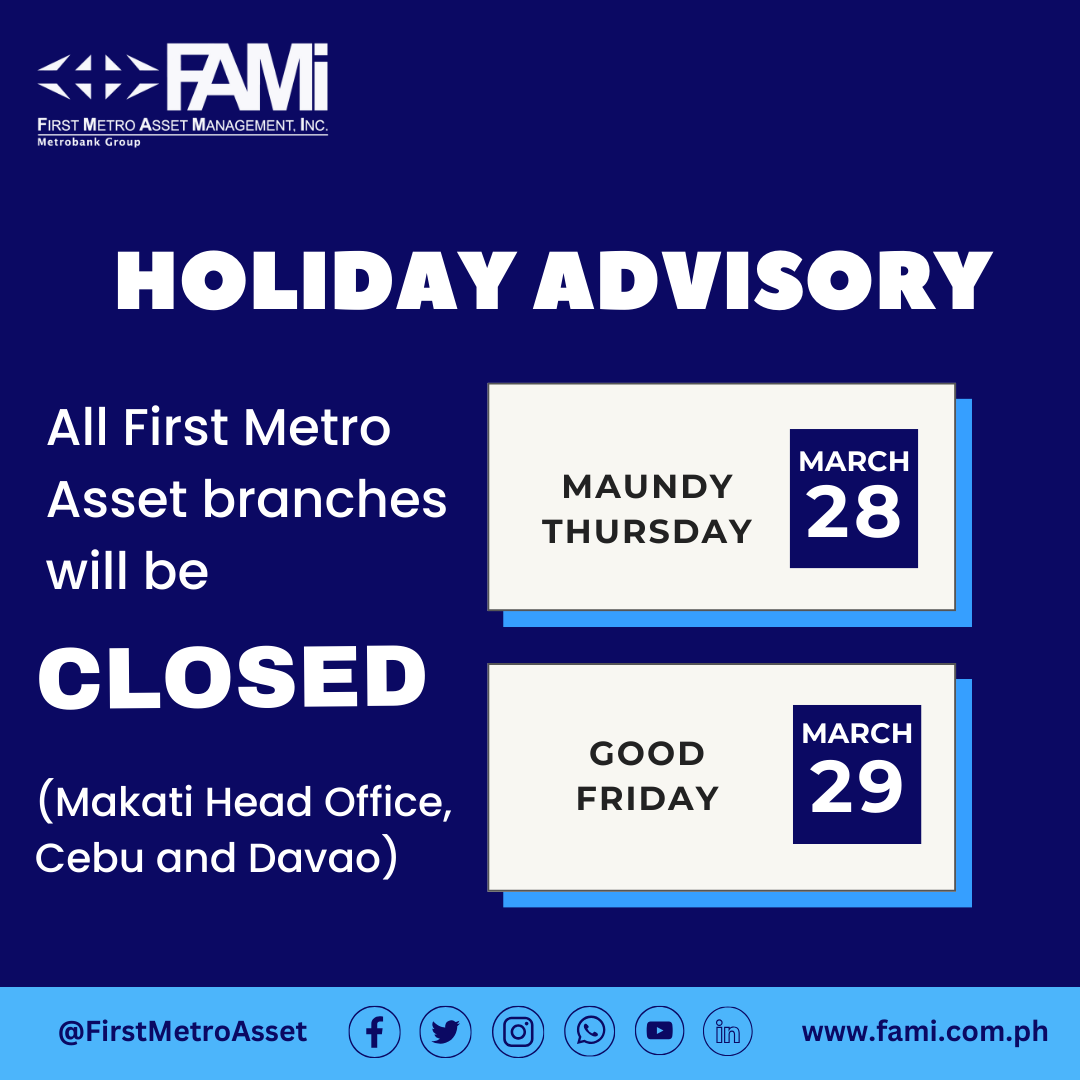

Holiday Schedule - Holy Week

Insights and Announcements

FACTORS AND FORCES OF INVESMENT WEBINAR February 4, 2023

Insights and Announcements

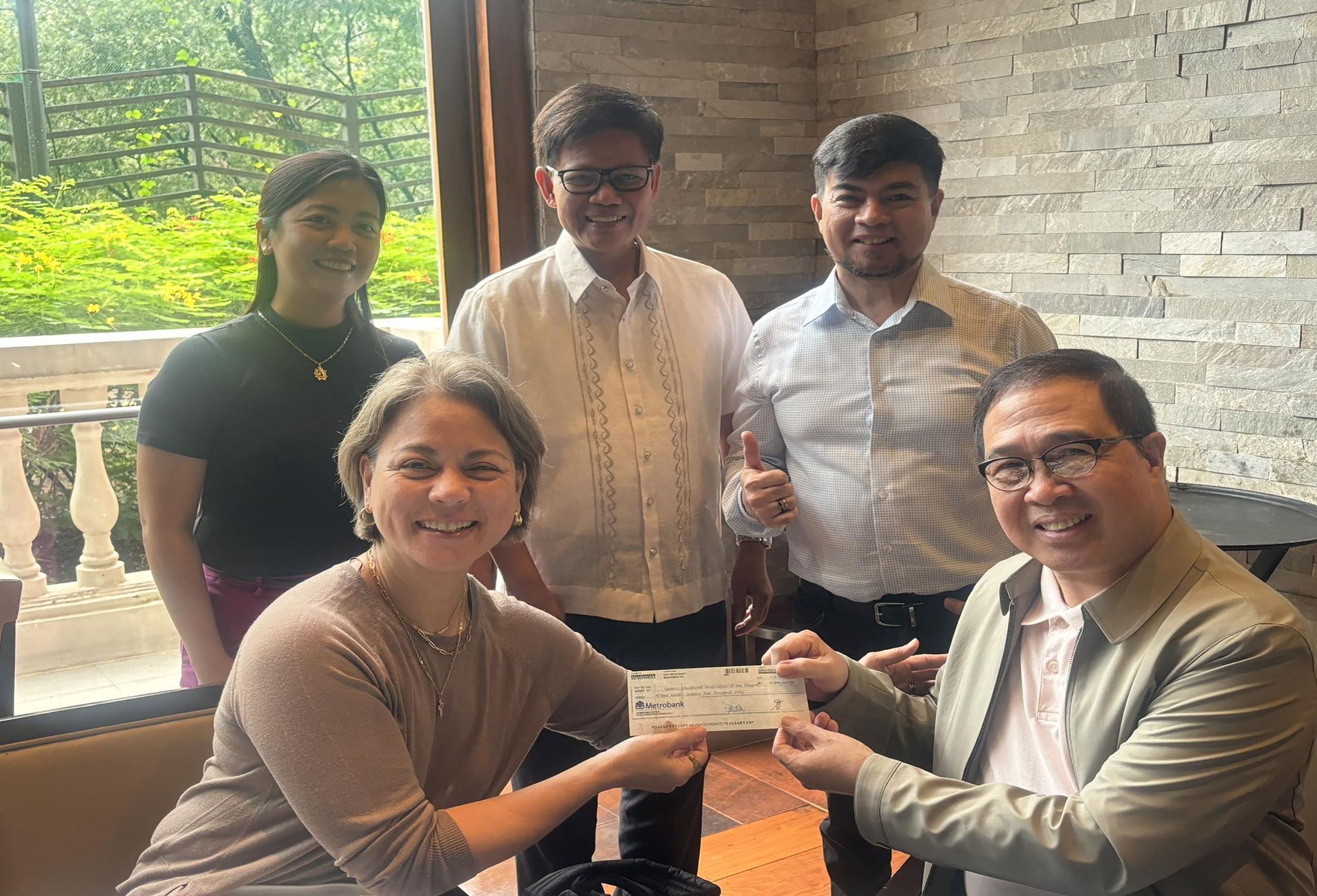

FAMI Releases Php 15 Million in Dividends to Partner Institution CEAP