Angelo Silva

Jun 06, 2018

4 mins

Rangebound on Higher Inflation Expectation

Outlook. We expect the bond market to sell amid the inflation news that portend of higher interest rates, keeping the yield curve firm to elevated this week. This is amid the release of May inflation number at the low end of the BSP inflation forecast band of 4.6% - 5.4%. May headline inflation spiked to a 5-yr high of 4.6% from 4.5% in April, but lower than the Department of Finance’s 4.9% forecast. While inflation was expected to taper off, market is hardly convinced rates have already peaked for the year. Inflation could continue to rise in the next three months due to base effects, global crude oil volatility and weak peso, although these may be largely priced in following the BSP’s 2018 guidance of a high inflation rate of 4.6% in 2018. On the other hand, the passage of a law that would ease imported rice quotas (and sequentially damp rice inflation) in July and a second rate hike by the BSP could temper pressure on the yield curve. Downside risks to inflation include higher-than-expected petroleum product price moves and further peso weakness. The global trade war threat also heightens worries about currencies already reeling from gaps in the trade and balance of payments positions.

Market review. The local benchmark yield curve rose by 6bps week-on-week (WoW) on average and up by 65bps year-to-date (YTD). The spread between the local 10-yr local benchmark and the 10-yr US Treasury (UST) stayed at 319bps last week as the former fell by 3bps to 6.08% (done) and up by 38bps YTD, while the latter was also down by 4bps WoW to 2.89%. Yields of ROPs fell by an average of 2bps, tracking USTs which likewise shed 1bp on average.

Average total daily traded volume down 45% week-on-week (WoW) to Php6.2bn. The liquid yield curve rose by an average of 4bps WoW. The front-end (364-day T-bill) rose by 7bps to 4.12%%, the belly (FXTN 10-61: 9.7yrs) rose by 18bps to 6.20%, while the tail (R25-01: 20.5yr) shed 8bps to 7.14%. Secondary trading average volume down by 45% WoW to Php6.2bn as T-bill volume decreased by 66% to Php1.6bn. On the other hand, T-bond average volume fell by 28% to Php4.6bn. The BTr’s latest Php66bn auction of 3-yr retail treasury bond (RTB) was fully-awarded and was 1.4x oversubscribed. Accepted bids averaged at 4.8%. Lastly, the latest Php15bn auction of 91-day, 182-day, and 364-day T-bills was only partially-awarded despite being twice oversubscribed. Average accepted rates for the 91-day and 182-day T-bills were 3.296% and 3.677%, both lower than the previous auction, but the accepted bid rates for the 364-day was capped at 4.246%.

Emerging Markets’ (EM) 10-year up 9bps week-on-week (WoW). Yields of EM bonds we follow were up by 9bps WoW on political news from the EU’s Italy conundrum and the U.S. imposing tariffs on steel and aluminum from the EU, Canada, and Mexico. Indonesia (10-year yield -7bps), the Philippines (-2bps), and Per (-3bps) outperformed last week, while Brazil (10-year yield +41bps), Turkey (+19bps), and Mexico (+12bps) underperformed.

USTs down 1bp WoW. US Treasuries were unchanged, down by just 1bp WoW on average, while the 10-yr UST shed 4bps WoW to 2.89%. UST yields are expected to rise this week following the May employment report that showed continuing strength in the labor market. The report said that the economy added a better-than-expected 223,000 jobs (vs 188,000 expected) last month. The unemployment rate declined to 3.8%, an 18-year low, from 3.9% in April. Average hourly earnings rose by 0.3%, slightly better than expected (0.1%), yielding an annualized rate of 2.7%. Jobs numbers are closely watched to see if labor market tightness would translate to wage growth, which in turn could spur inflation. Elsewhere, trade turmoil between the U.S. and other nations continued to keep markets jittery. Last week, the U.S. administration implemented metal tariffs on Canada, Europe and Mexico, a move that was widely criticized, although the US maintained that it still wants strong ties with these countries. Investors will turn their attention to the manufacturing index numbers to be released this Tuesday (Wednesday, PH time) and the G-7 summit with the heads of Canada, Japan, German, France, the U.K. and Italy in attendance.

Read full article here.

Related Articles

Insights and Announcements

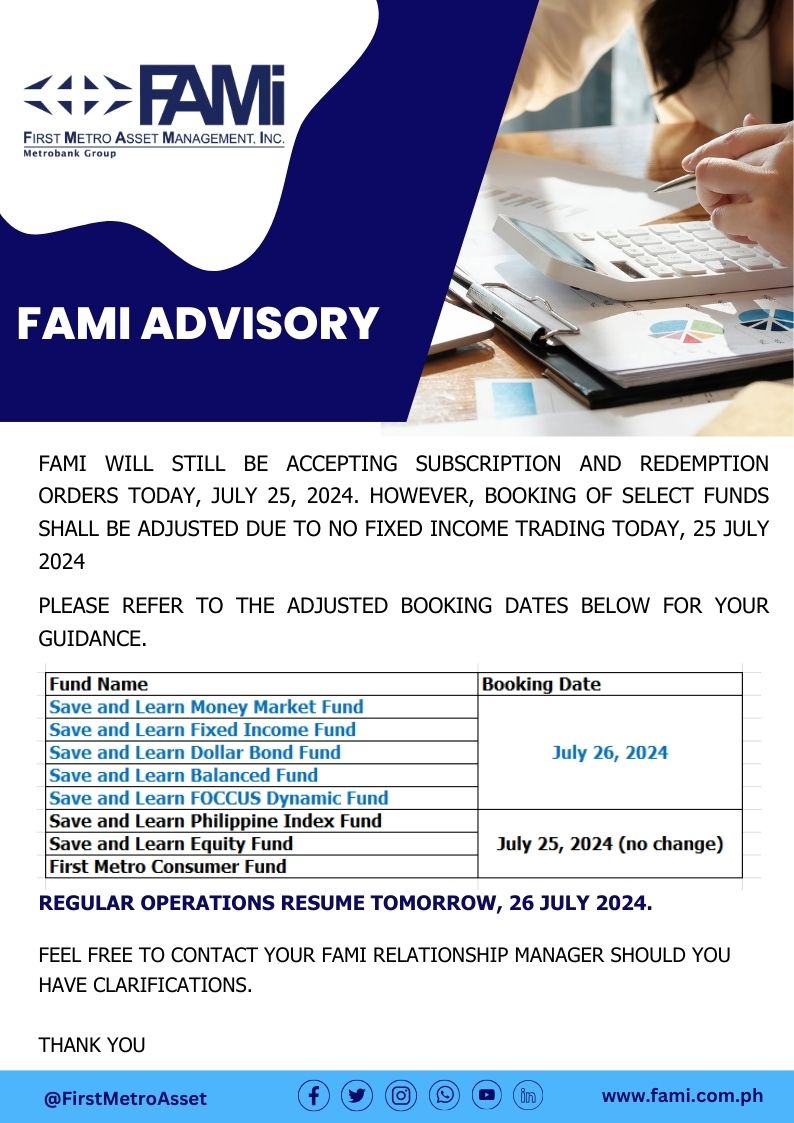

FAMI BOOKING ADVISORY