Angelo Silva

May 22, 2019

4 mins

Liquidity Rally

Outlook. Profit taking ensued in the bond market last week following the Bangko Sentral’s (BSP) widely-expected decision to cut the reserve requirement ratio (RRR) by 200bps, which will happen on a staggered basis (100bps in May 31, 50bps by June 28, 50bps by July 26). However, we expect downtrend to resume especially in the short end, where yields for the 1-yr benchmark (5.97%) is still higher than the 10-yr (5.79%). The cut, which is expected to release Php180-200bn into the financial system, together with the earlier 25-bp policy rate cut was meant to stimulate the economy that slowed to a 5.6% growth in the first quarter.

The Bureau of the Treasury (BTr) successfully issued its second batch of panda bonds last week. A total of RMB2.5bn with a tenor of three years was well-received, garnering a bid-to-cover ratio of 4.4x. The paper was priced at 3.58%, just 32bps above the benchmark rate. The auction closely followed the government’s $842.3mn 8-year euro bond sale in the prior week. Amid heightened US-China trade noise, there could be some leftover profit taking in the local bond market after it sank by an average of 20bps in the past month, but the prevailing trend is still downward.Market review. The local benchmark yield curve fell by 2bps on average week-on-week (WoW) following the RRR cut. The spread between the local 10-yr local benchmark and the 10-yr US Treasury (UST) widened to 340bps from 328bps in the week prior as the former rose by 4bps WoW to 5.79%, while the latter shed 7bps to 2.39%. Year-to-date, the local yield curve was down by an average of 112bps while the 10-yr was down by 128bps. Yields of ROPs were flat on average while US Treasuries were down by 6bps on average.

Average total daily volume flattish, up by just 3% week-on-week (WoW) to Php24.2bn. The liquid yield curve fell by an average of 1.9bps WoW as the front-end (364-day T-bill) was down by 9bps to 5.97%, the belly (FXTN 10-63: 9.5yrs) up by 4bps to 5.79%, while the tail (R25-01: 20.5yr) was flat at to 5.95%. Secondary trading average volume fell was flattish, up by just 3% to Php24.2bn ahead of the expected RRR cut. T-bill volume more than doubled up to Php7.8bn while T-bond fell by 19% to Php16.4bn. The Bureau of the Treasury’s (BTr) fully awarded its latest Php20bn auction of reissued 7-year T-bonds at an average yield of 5.743%, 19bps lower than its initial issue last February. The auction was 2.5x oversubscribed. Lastly, the latest Php15bn auction of 91-day, 182-day, and 364-day T-bills was fully awarded at average rages of 5.258%, 5.700%, and 5.869%, respectively, 13bps, 9bps, and 7bps lower than the previous auction. The auction was 3.35x oversubscribed.

Emerging Markets’ (EM) 10-year down 5bps (WoW). Yields of EM bonds we follow were down by 5bps on average as EM markets remained hostage by global trade tensions. Turkey (10-year yield -26bps), Colombia (-9bps), and Indonesia (-5bps) outperformed last week, while Chile (10-year yield -1bp) and Peru (-1bp) underperformed.

USTs down 6bps WoW. US Treasuries were down by 6bps WoW on average as the 10-yr UST likewise fell by 8bps to 2.39%, amid heightened trade tensions with China. China retaliated last week and announced that it was imposing $60bn in tariffs on US imports after the US’ tariff hike on $200bn Chinese imports in the prior week. Odds for a cut this year continue to fall as indicated by Fed futures prices. A December cut remains the likeliest but the odds have steadily fallen from 50+% last March to just 43% last week due to the inflationary effects of the tariff hikes. The market will turn its attention to the release of Fed minutes on Wednesday (Thursday, PH time) and a full slate of Fed speakers throughout the week. Recall that the Fed was decidedly dovish following its May 1 meeting, but economic data released after that have been encouraging.

Read full article here.

Related Articles

Insights and Announcements

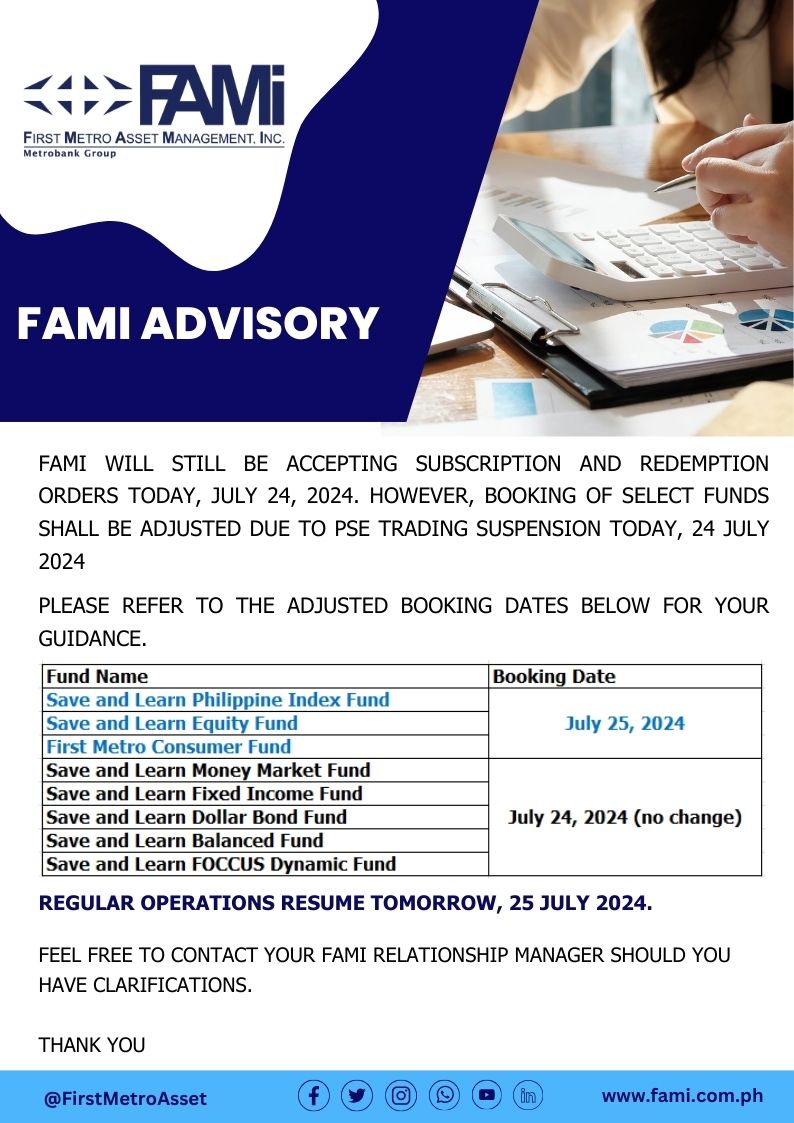

FAMI BOOKING ADVISORY