Angelo Silva

Jun 19, 2018

4 mins

Will BSP Follow Second Fed Hike?

Outlook. We expect bond yields to remain elevated this week ahead of the expected Fed hike this Thursday (PH time). U.S. inflation also accelerated in May by 2.8% year-on-year (YoY), the fastest pace in more than six years, reinforcing the Fed’s outlook for gradual interest rate hikes while eroding wage growth that remains subdued despite an 18-year low in unemployment. This will be the second of the three hikes projected by the Fed this year. With gross international reserves (GIR) level falling to a 3-year low last May to $78.97bn from $79.61bn in April, the peso-dollar rate fell to a 12-year low of Php52.95 last Monday. A hike by the Bangko Sentral ng Pilipinas (BSP) could prevent the peso from weakening any further, a decision that could be made in the next monetary board meeting this June 21. Meanwhile, the local yield curve flattened following the Php121bn sale of 3-year retail treasury bonds (RTB) last week at a coupon rate of 4.875%. Inflation expectation remains elevated despite last May’s inflation settling at the lowest end of the BSP’s 4.6%-5.4% expectation. Near-term upward inflationary pressure brought about by TRAIN kept yields in the short-end to the belly elevated, while tempered long-run GDP expectation due to lack of progress with the infrastructure program kept tail-end yields under pressure.

Market review. The local benchmark yield curve fell by 3ps week-on-week (WoW) on average and up by 63bps year-to-date (YTD). The spread between the local 10-yr local benchmark and the 10-yr US Treasury (UST) narrowed to 315bps from 319bps last week as the former stayed at 6.08% (done) and up by 38bps YTD, while the latter rose by 4bps WoW to 2.93%. Yields of ROPs rose by an average of 2bps, tracking USTs which increased by 3bps on average.

Average total daily traded volume down 12% week-on-week (WoW) to Php5.4bn. The liquid yield curve fell by an average of 2bps WoW. The front-end (364-day T-bill) rose by 6bps to 4.18%%, the belly (FXTN 10-61: 9.7yrs) fell by 23bps to 5.97%, while the tail (R25-01: 20.5yr) shed 39bps to 6.75%. Secondary trading average volume fell by 12% WoW to Php5.4bn as T-bond volume decreased by 44% to Php2.6bn. On the other hand, T-bill average volume rose by 75% to Php2.9bn, reflecting investors’ defensive with their preference of short-term notes. The BTr’s latest Php66bn auction of 3-yr retail treasury bond (RTB) was raised again to Php121.8bn amid robust appetite for the paper. The original offer was Php30bn. Meanwhile, the latest Php15bn auction of 91-day, 182-day, and 364-day T-bills was only partially-awarded despite being 1.6x oversubscribed. Average accepted rates for the 91-day and 182-day T-bills were 3.323% and 3.714%, higher than the previous auction but lower than secondary market rates, while the accepted bid rates for the 364-day was capped at 4.324%, higher than the previous auction.

Emerging Markets’ (EM) 10-year up 6bps week-on-week (WoW). Yields of EM bonds we follow were up by 6bps WoW amid geopolitical noise and ahead of the G-7 summit in Canada over the weekend. Thailand (10-year yield -7bps), Taiwan (-7bps), and Colombia (-6bps) outperformed last week, while Brazil (10-year yield +69bps), South Africa (+35bps), and Indonesia (+31bps) underperformed.

USTs up 3bps WoW. US Treasuries rose by an average of 3bps last week, while the 10-yr UST also increased by 4bps WoW to 2.93%, ahead of the expected Fed hike this week and the G-7 summit over the weekend. Bond investors widely expect the U.S. central bank to raise key overnight borrowing costs by a quarter point to 1.75-2.00%, while market will tune into the policymakers’ tone whether there will be one or two hikes in the second half. Meanwhile, analysts and traders are likewise looking for signs on whether the European Central Bank (ECB) is prepared to begin tapering its 2.55tn euro bond purchase program in September amid the recent market turbulence tied to political turmoil in Italy

Read full article here.

Related Articles

Insights and Announcements

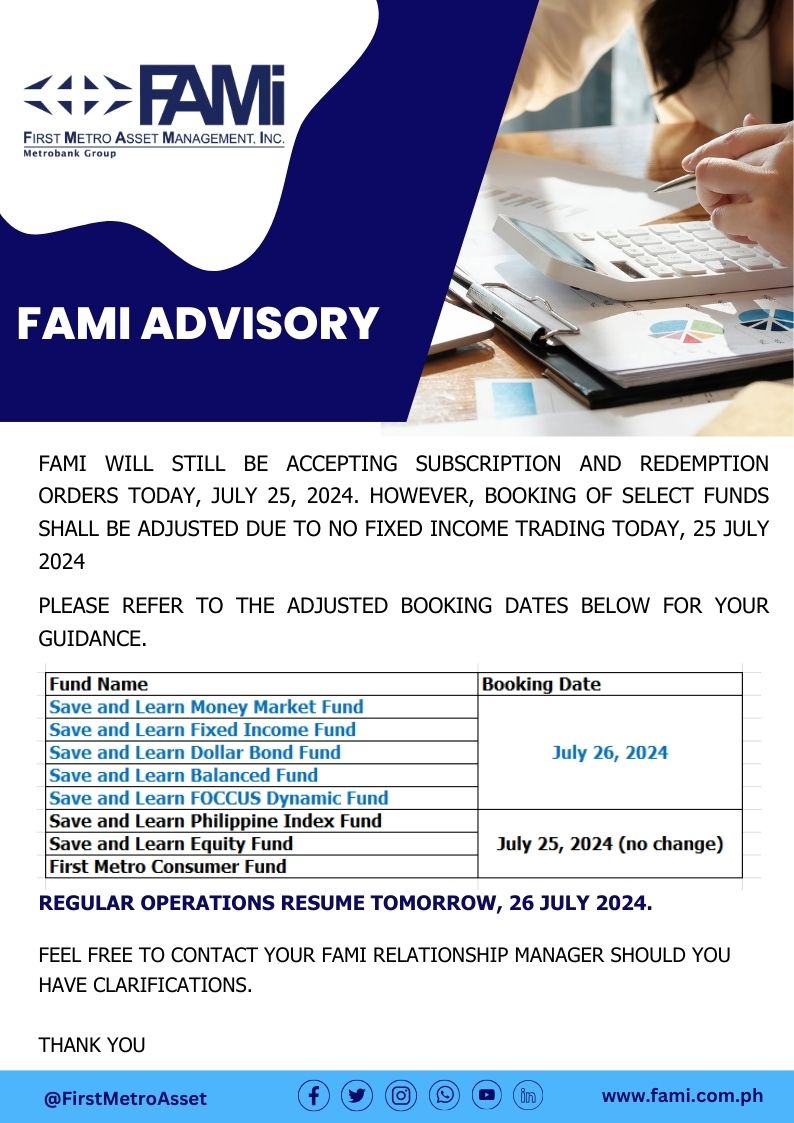

FAMI BOOKING ADVISORY

Insights and Announcements

2022 Annual Shareholders Meeting of First Metro Asset Management, Inc.