Angelo Silva

Aug 01, 2018

4 mins

Accelerating Inflation

Outlook. Expectations of 1) a Bangko Sentral ng Pilipinas (BSP) rate hike in August spurred by rising inflation expectations, and; 2) faster US economic growth in the past quarter drove local benchmark yields higher by an average of 11bps last week. The BSP expects July inflation to rise between 5.1%-5.8%, higher than June’s 5.2% and the Department of Finance’s (DoF) 5.3% forecast. During the prior week, Standard Chartered reported its August inflation to rise by 5.8%. We expect yields to go sideways this week as the market anticipates the ‘strong monetary adjustment’ indicated by BSP governor Espenilla last week, but a strong upward bias remains.

Meanwhile, the US gross domestic product (GDP) rose by 4.1% in the second quarter from 2.2% in the first quarter, just a tad short of the expected 4.3% by analysts surveyed by Bloomberg but still the fastest pace since 2014. Consumer (+4.0%) and business (+7.3%) spending as well as a surge in exports (+5.7%) in anticipation of retaliatory tariffs by China drove economic growth.Market review. The local benchmark yield curve rose by 11bps week-on-week (WoW) on average and up by 104bps YTD. The spread between the local 10-yr local benchmark and the 10-yr US Treasury (UST) widened to 369bps from 351bps in the prior week as the former rose by 26bps to 6.65% (bid), while the latter was higher by 7bps WoW to 2.96%. Yields of ROPs also rose by an average of 2bps, tracking the movement of the UST curve which was 5bps higher on average last week.

Average total daily traded volume down 36% week-on-week (WoW) to Php5.0bn. The liquid yield curve rose by an average of 10bps WoW as the market braced for an almost certain BSP hike on August 9. The front-end (364-day T-bill) rose by 12bps to 4.82%, the belly (FXTN 10-61: 9.7yrs) likewise increased by 24bps to 6.60%, while the tail (R25-01: 20.5yr) rose by 6bps to 7.39%. Secondary trading average volume fell by 36% to Php5.0bn, dragged by a 44% drop in average T-bond volume to Php2.0bn. T-bill trading, likewise, dipped by 29% to Php3.0bn. Last Monday, the latest Php15bn auction of 91-day, 182-day and 364-day T-bills was fully-awarded as demand was healthy in the short end of the curve. Average T-bill rates settled at 3.261%, 4.294%, and 4.900%, respectively, 50bps, 60bps, and 10bps higher than the previous auction, and was 2.4x oversubscribed. On the other hand, the Bureau rejected all bids for the reissued 10-yr bond with bid rates reaching an average of 7.390%, higher than the previous auction. The auction was 1.3x oversubscribed for the Php15bn offered.

Emerging Markets’ (EM) 10-year flat (WoW). Yields of EM bonds we follow were unchanged WoW on average amid expectation of a tighter monetary policy in Japan and the European Central Bank (ECB) keeping interest rates steady last Thursday, with ECB President Mario Draghi not signalling any change to the forward policy on ending bond purchases at the end of the year. South Africa (10-year yield -15bps), Hungary (-14bps), and Indonesia (-13bps) outperformed last week, while Turkey (10-year yield +72bps), the Philippines (+26bps), and Argentina (+15bps) underperformed.

USTs up 5bpsWoW. US Treasuries rose by 5bps WoW on average, while the 10-yr UST was up by 7bps WoW to 2.96%, as the US GDP rose at its highest pace since 2014 in the second quarter at 4.1%. Also, last week, Trump and European Commission President Juncker announced plans to negotiate the elimination of tariffs on non-auto industrial goods as well as a promise to increase imports of US soybeans, which the market took as a de-escalation of tensions between the US and the EU. This was certainly a relief after weeks of noise surrounding the US and major trade partners like China and Iran. Meanwhile, no rate hike is expected as the Fed meets this Tuesday-Wednesday (Wed-Thu, PH time), but analysts made it clear that this was not because of Trump’s previous bashing of the Fed’s rate hikes. Fed Chair Powell reiterated the course of a gradual rate hike, while the strong 2Q GDP numbers cemented the possibility of rate hike this September, with odds rising to 89% from 83% prior to the release. Odds for a December hike also rose to 63% from 59%, although there is also a possibility that the spike in exports will be shrugged off due to anticipatory moves by soybean exporters ahead of possibility retaliatory tariffs by China.

Read full article here.

Related Articles

Insights and Announcements

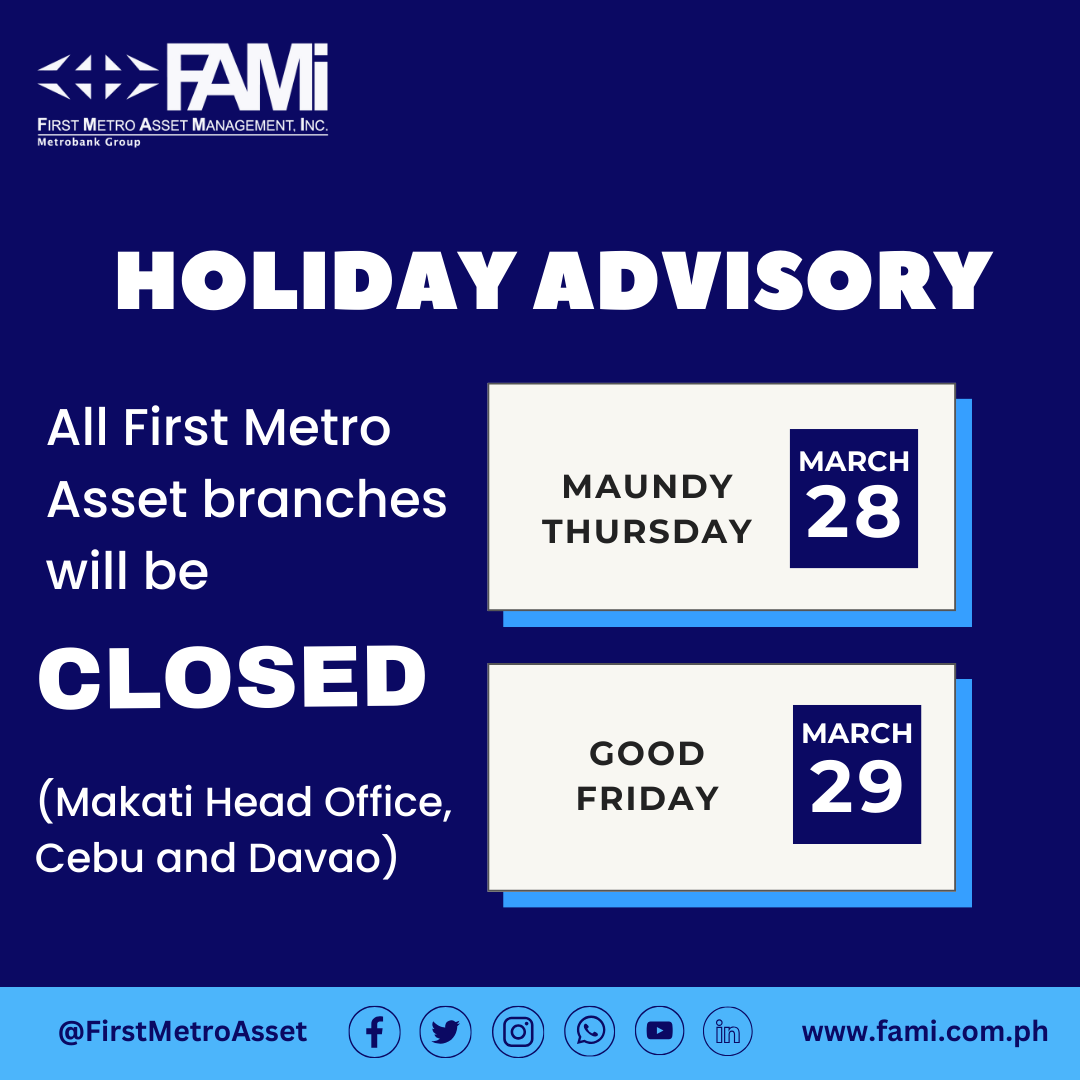

Holiday Schedule - Holy Week

Insights and Announcements

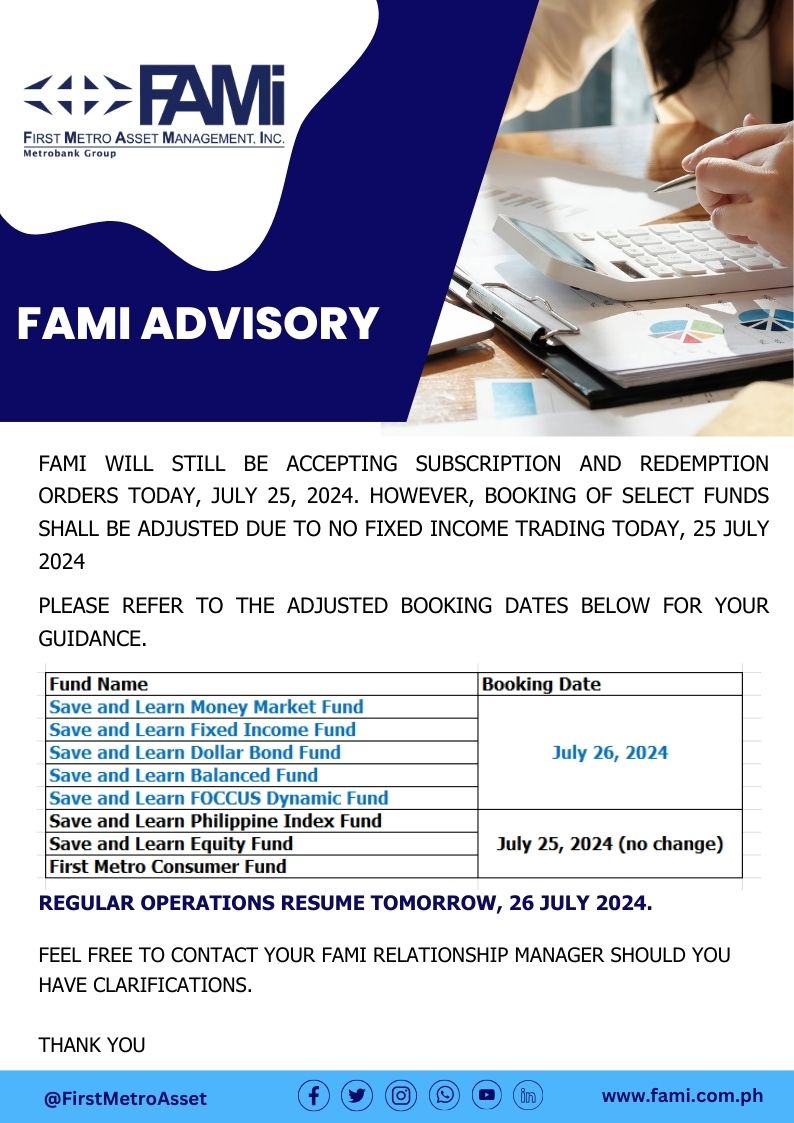

FAMI BOOKING ADVISORY