Angelo Silva

Aug 14, 2019

2 mins

Liquidity Easing

Outlook. Interest rates are moving lower on liquidity easing by the BSP, a trend likely to be sustained, also on the back of lack of news about an aggressive return by the government back to the bond market. Foreign borrowing was just concluded with the Samurai bond float this month worth Php44bn, which raised the foreign reserves buffer of the BSP to $85b, equal to 7.4 months’ worth of imports and 5.2x cover for short-term liabilities.

The peso yield curve went down by 45 bps on the average for the entire month of Aug. to date and was lower at 2.93% from the year’s start (tenor above 1 yr) and 270 bps lower on the average from the October peak for tenors above 1 yr.Market review. The local benchmark yield curve and US Treasuries both fell 35bps and 9.1bps on average week-on-week (WoW), respectively. Year-to-date, the former was down by 284bps following the central bank’s decision to cut benchmark interest rates and has further eased due to another possible 25bps cut and 1 percentage point cut in RRR. The front-end (364-day T-bill) dropped 43bps to 3.72%, the belly (FXTN 10-63:9.5yrs) down 21bps to 4.37%, while the tail (R25-01:20.5yr) shed 21bps to 4.70%, all WoW.

Liquidity Indicators. Gross international reserves (GIR) rose to $85.18bn in July from $84.93bn in June. BSP reported that the increase in GIR was due to inflows arising from the BSP’s foreign exchange operations and income from investments abroad and the National Government’s net foreign currency deposits.

For the week July 25-31, 2019 (latest week), time deposits for below 1 year, 1-2 years, and over 2 years were at 3.7%, 3.5%, and 4.3%, respectively. It dropped by 0.2%, 0.2%, and 0.3%, respectively from the previous week. Meanwhile, for the week July 29-August 2, 2019 (latest week), Interbank Call Loan Rate was at 4.65% from 4.72% of the previous week. Read full article here.

Related Articles

Insights and Announcements

2023 Macro Economic, Equities and Fixed Income Outlook

Insights and Announcements

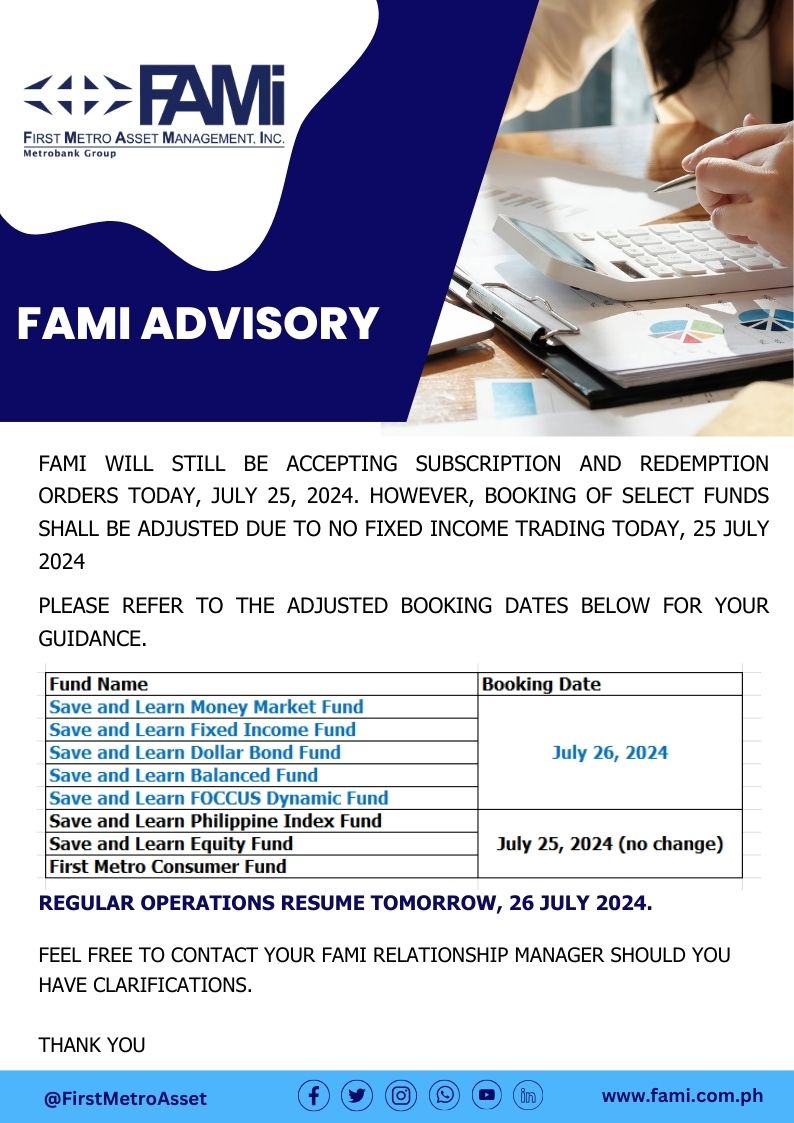

FAMI BOOKING ADVISORY

Insights and Announcements

2022 Annual Shareholders Meeting of First Metro Asset Management, Inc.