Angelo Silva

Sep 04, 2019

4 mins

Less Than 2% August Inflation: Ten Years Headed Lower

Outlook. Lower inflation rate guidance by the Bangko Sentral ng Pilipinas (BSP), 1.3-2.1% for last month, is not helping much to push down the ten year rate which continues to hover around 4.2%-4.4%. Some big banks are locking in profits, selling huge profitable positions and that’s keeping secondary rates steady and unable to break below 4%, which many view to be a critical support and where interest rates are bound to approach ahead of more policy rate cuts and triple R cut by the monetary authorities.

Pricing In. But the short-end of the curve is much more responsive. The Bureau of the Treasury (BTr) fully awarded its Php15bn auction of 92-, 183- and 365-day T-bills at an average yield of 3.149%, 3.429%, and 3.659%, respectively, lower than the previous auction results of 3.254%, 3.471%, and 3.636%. The auction was oversubscribed with total bids reaching Php40.3bn. BTr also awarded the reissued 3-year Treasury Bonds, which fetched an average rate of 3.961%, nearly thrice oversubscribed on total tenders of Php56.6bn.

August Inflation on Radar Screen. Rates await the August inflation and if it comes out below 2%, our guess (Research Dept.) is 1.6%, then rates may affirm the consensus market view that the peso yield curve has further to fall. FMIC’s house view is for the the 10 year rate to dip to 4% by yearend on the back of the ff: lower inflation in the third quarter (less than 2%), more policy rate cuts (25 bps and 2% cut in the triple R until yearend plus), a sure 25 bps cut in Fed policy on Sept. 18.

No Crowding Out. There’s also no indication of any upcoming big government borrowing that can potentially crowd out private debt. But goverment spending appears to be gaining steam, up in July by 23% to Php339bn month-on-month. However, year-to-date, government spending is yet to make a big leap as it was just up 3% to Php1.929tn due to the legislation hitch. Against government revenues that were up 10% to Php1.811tn in the same period, the budget deficit fell to Php118bn, down by 57.8% versus Php279.4bn of the same period in 2018. For the month of July, the budget deficit was 12.83% lower than last year to Php75.3bn.

Slow-moving Projects. The opposition in the Senate aired their dismay over the slow-moving government pumppriming, noting that only 11 out of the planned 75 projects were either completed or are still ongoing. Government’s public investment program now tops more than 9,800 infrastructure projects nationwide until the year 2022, with total value of Php10.98tn.

US Treasuries and Local 10 yrs Bond. The local benchmark yield curve and US Treasuries (UST) both fell 34 bps and 5 bps on average week-onweek (WoW), respectively. The peso ten-year rate fell to 4.46% as of yesterday, down by 2 bps versus Aug. 23; also the 10 year UST was lower by 2 bps to 1.5%. Year-to-date, the peso ten year government bond was down by 282 bps. Week on-week, the front-end (364-day T-bill) was up by 1 bp to 3.69%; the belly (FXTN 10-63:9.5yrs) was steady or down 2 bps to 4.46%, while the tail (R25-01:20.5yr) shed 2.1 bps to 4.83%. Secondary trading average volume was up 34.5% to Php22.8bn, while T-bill volume down 14.1% to Php4.6bn.

Liquidity Indicators: Still Tight. Time deposit (TD) rates for short-term (below one year tenor) were down to 4.158% in July while long-term TD rates was up 8 bps to 4.668% in July from 4.588% of the previous month. And this reflected the stickiness of the downward rates even with the BSP’s talk on policy rate cuts. Interbank Call Loan Rate (IBCLR) was down to 4.773%, lower by 16 bps from 4.937% of the previous month, still above the policy rate of 4.25% which indicates financial system tightness, still.

Read full article here.

Related Articles

Insights and Announcements

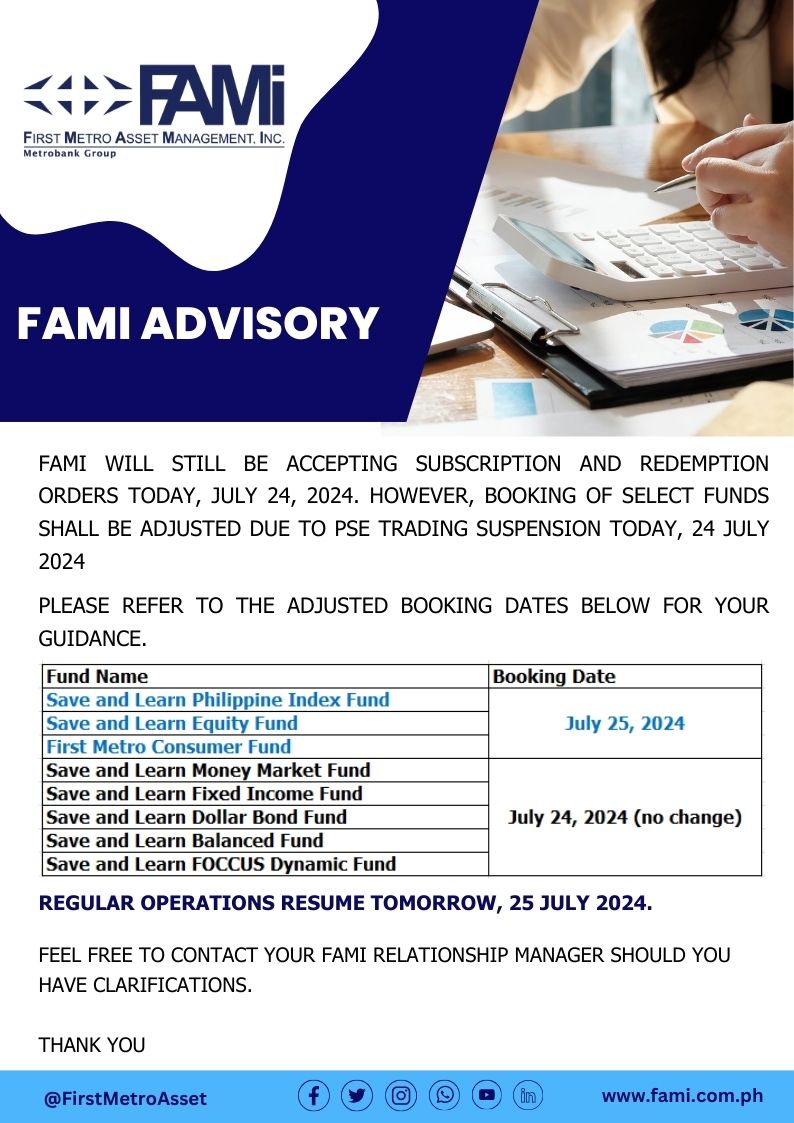

FAMI BOOKING ADVISORY