Angelo Silva

May 02, 2018

4 mins

Eyeing a BSP Hike

Outlook. We expect local bond yields to remain elevated as the market is somewhat unanimous in its reading of the Bangko Sentral ng Pilipinas’ (BSP) recent signal of its readiness to hike rates in its next policy meeting. Banks are predicting that the BSP will hike at least once and as soon as its meeting on May 10 to curb a rapidly rising local inflation. April inflation will be released on Friday and is expected to hit 4.5% from 4.3% in March. Furthermore, US Treasury (UST) yields are on the rise with the 10-yr UST breaching the 3.0% mark last week for the first time in four years following the release of stronger-than-expected US 1Q18 GDP that clocked in at 2.3% versus 2.0% expected and 2.9% in the fourth quarter despite consumer spending growing at its slowest pace in five years (at 1.1% from 4.0% in 4Q17). A rally in oil and other commodity prices, fresh UST supply totalling $96bn last week, and renewed inflation expectation buoyed UST yields. Trump’s determination to end the Iran denuclearization deal sent oil futures soaring to $90/barrel, which could lead to higher local inflation expectations and put the BSP’s non-action into question. The immediate consideration is that supplies have tightened and steady depletion of stockpiles. OPEC compliance to its output cut agreement exceeded targets, and Venezuelan output has been halved over the past two years to levels not seen in a more than a decade. Speculation that the US could re-impose sanction on OPEC’s third largest producer, Iran, as early as May 12, is also cited as a factor. Estimates of the impact of this speculation range between $1-$3/bbl.

Market review. The local benchmark yield curve was up by 5bps week-on-week (WoW) and 65bps year-to-date (YTD) as USTs remained elevated last week. The spread between the local 10-yr local benchmark and the 10-yr US Treasury (UST) slightly narrowed to 325bps from 328bps last week as the former fell by 4bps to 6.21% and up by 51bps YTD, while the latter was flat WoW at 2.96%. Yields of ROPs rose by an average of 8bps as USTs were unchanged WoW. Total daily traded volume up 39% week-on-week (WoW) to Php7.6bn. The liquid yield curve fell by 1bp on thin trading last week. The front-end (FXTN 05-72: 1yr) fell by 11bps to 3.44%, the belly (FXTN 10-61: 9.7yrs) was unchanged at 6.07%, while the tail (R25-01: 20.5yr) rose by 7bps to 7.17%. Secondary trading volume increased by 39% to Php7.6b, still on the low-end of trading volume. T-bill trading reached Php4.0bn, up 29% week-on-week (WoW) and the highest level this year, while T-bond trading volume rose by 53% to Php3.6bn. Defensiveness still dominate the bond market as investors still opted for shorter-tenored notes, resulting in a steeper yield curve. The BTr fully awarded its Php5bn 91-day T-bill auction yesterday (April 30) while partially awarding the bids for the 182-day and completely rejecting all bids for the 364-day bill as bid rates trended higher than expected. Average bids for the 91-day bill was capped at 3.49%, 10bps lower than the previous auction’s 3.59%. On the other hand, accepted bid rates for the 182-day were capped at 4.02%. The auction was 1.6x oversubscribed.

Emerging Markets’ (EM) 10-year yields up 10bps week-on-week (WoW). Yields of EM bonds we follow were up by 10bps WoW on average amid Brent and WTI oil prices retracing previous highs of $82/bbl and $76.5/bbl, respectively. Brazil (10-year yield +7bps), the Philippines (+7bps), and Chile (+7bps) relatively outperformed last week, while Colombia (10-year yield +15bps), Indonesia (+12bps), and Turkey (+13bps) underperformed.

USTs flat WoW. US Treasuries were unchanged on average WoW, while the 10-yr UST also held steady at 2.96% despite breaching the 30% intra-week. First quarter GDP slowed to 2.3% from 2.9% in 4Q17, but was faster than expectations of 2.0%. Fed officials are expected to shrug off the tepid first quarter reading as it it usually seasonally sluggish. Economists expect growth will accelerate in the second quarter as households start to feel the impact of the $1.5tn income tax package on their paycheck, which came into effect last January. The FOMC is also widely expected to hold rates (94.3$ odds to hold) in their next policy meeting on May 2 (May 3, PH time) but expects a hawkish tone as wages and the overall employment landscape remain robust, while the outlook for US economic growth remains substantially optimistic. The positive impact of fiscal stimulus in the form of tax cuts has yet to be determined, but will likely serve as a tailwind for the economy going forward.

Read full article here.

Related Articles

Insights and Announcements

2023 Macro Economic, Equities and Fixed Income Outlook

Insights and Announcements

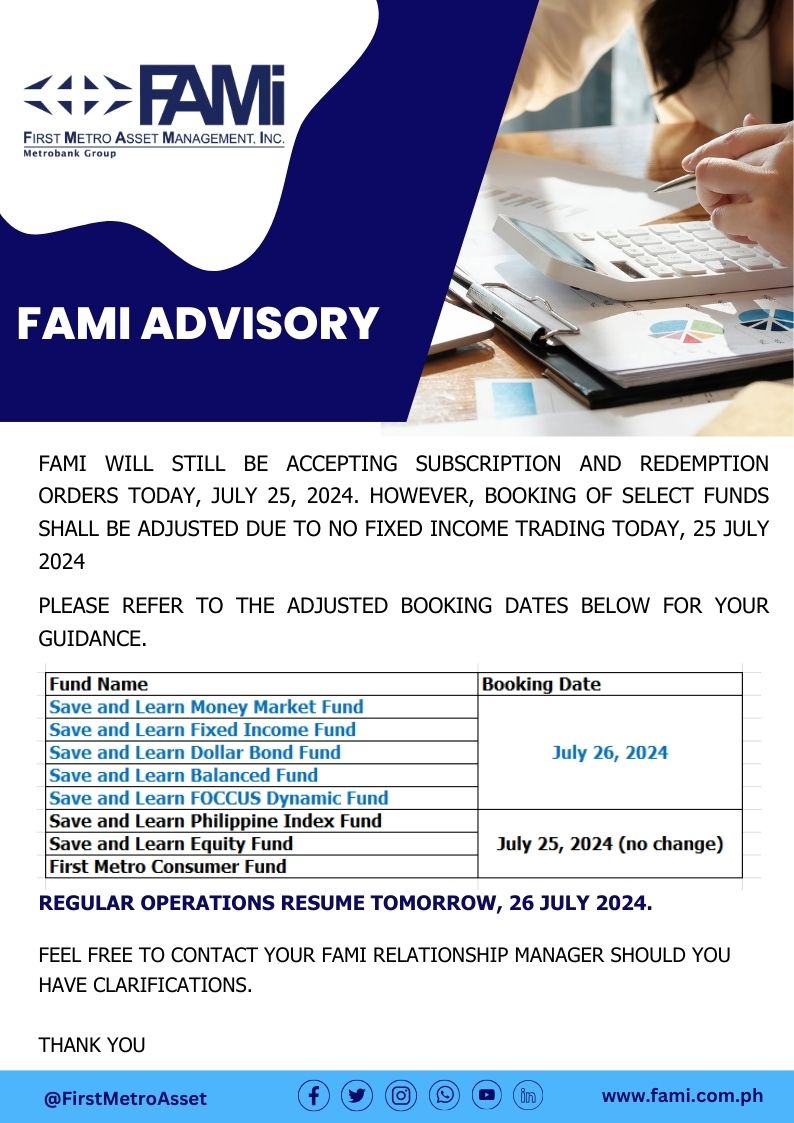

FAMI BOOKING ADVISORY