Angelo Silva

May 29, 2019

4 mins

Equities Outlook

Outlook. We’re looking at the 7,600-7,800 range this week. MSCI rebalancing took effect yesterday (May 28,2019) which was expected to result in a $150m outflow from passive funds. Since the announcement (May 14,2019), the Philippine market saw $220m net foreign outflows but the index held on and even gained 1.31% as of Friday’s close. We think that the 7,600 will hold due to bargain hunting but the 7,800 might be hard to break in the absence of catalysts.

SCC was added to the small cap index, replacing CNPF. AC and ICT received the largest up weight while ALI and SMPH were down weighted. Also, FTSE announced its quarterly index review and Philippines was also down weighted to make room for China A-Shares. FTSE quarterly review will take effect on June 21, 2019.Market Review. The main bourse bounced 2.2% to 7,747.1 last week after two consecutive weeks of declines as investors bought beaten down conglomerates were bought up as it offered attractive valuation. Leading the charge were AEV, up 9.7%, followed by GTCAP which gained 7.7% as it bounced after being sold down due to a weak 1Q19 earnings result. LTG fell 11% as the government moved to rush the passing of a new set of sin taxes to finance the government’s universal health care program.

Market Flows. Foreigners continued to be net sellers for the third straight week, ahead of MSCI rebalancing. Net foreign selling was Php5.6bn for the week as selling pressure continued for JFC, AC, SM, SMPH, and BPI. Telco companies, namely GLO and TEL, were picked up by foreigners after outperforming earnings expectations in 1Q19.

Regional Markets. Equity markets continued their declines led by Hang Seng which fell by 2.1% w/w. Over the US, S&P 500 fell 1.2% while Dow Jones index fell 0.7% last week. Trade war continues to drag and the market is already braving for the worse, locking in gains ahead of Trump and Xi Jinping’s meeting in the G20 summit next month.

Currencies. The peso remained steady at Php52.18/$ and was able to recoup 0.9% w/w as the overhang on the monetary easing was lifted and the BSP provided more visibility in terms of policy direction.

Economic News

Foreign portfolio investments outflows for the month of April were $298.8mn almost wiping out year-to-date foreign portfolio investment down to $37.27mn ytd, after peaking at $1.15bn in the first week of March. Excluding Peso Time Deposits, all other asset classes saw outflows in April led by Peso Government Securities which saw $238mn in outflows while equities saw $61mn in selling.

Balance of Payment in the first four months was $4.3bn, almost a $6bn swing from the $1.5billion deficit in the same period last year. The BSP attributed the remittances and net inflow of foreign portfolio investment and net inflow of foreign direct investment in the first two months of the year. The government reported Php86.9bn surplus for the month of April which brought year-to-date deficit down to Php3.4bn. The surplus was due to the 15.1% decline in spending to Php221bn caused by the four-month budget impasse. Jan - Apr expenditure was Php999.8bn of the Php3.774tn budget for the year.Corporate News

Last week, we wrapped up corporate earnings for 1Q19. Overall, we think earnings disappointed with core net income of 5.2%, behind the 10% expectation. Conglomerates were dragged by their energy units and unlisted subsidiaries while the telco, property, and banking sectors outperformed.

Ayala Corp (AC) announced that it has acquired 3,805,644 shares at Php838/sh from Mitsubishi Corp, equivalent to 0.6% of AC’s outstanding shares and equal to Php3.2bn in foreign outflows that week. The sale was due to Mitsubishi Corp’s portfolio rebalancing exercise which brought its share of AC to 6% from 6.6%. Read full article here.

Related Articles

Insights and Announcements

FAMI Employees Join Forces in supporting FCC Women’s Run PH

Insights and Announcements

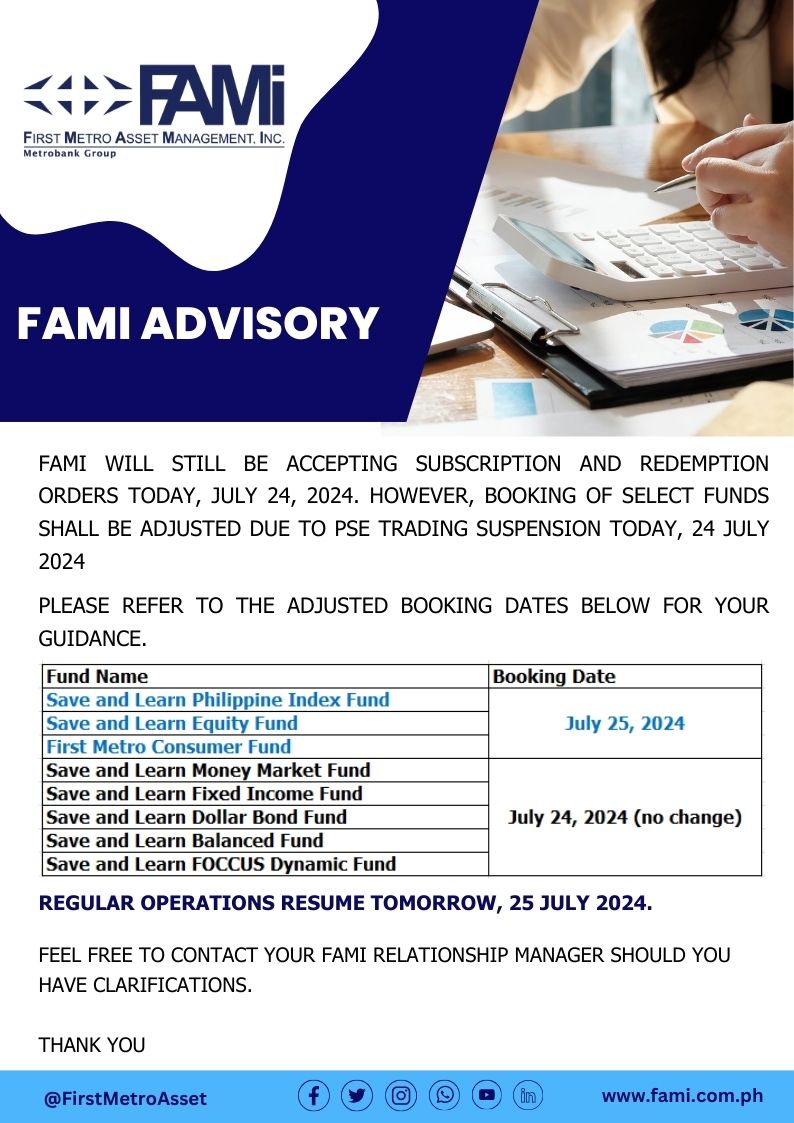

FAMI BOOKING ADVISORY