Angelo Silva

Jul 03, 2018

4 mins

Equities Outlook

Outlook. We expect the PSEi to be range bound at around 7,000-7,300 ahead of the June inflation release on July 5 (Thurs.), with bet at 4.7% year-on-year (y/y), slightly higher than May’s 4.6%. Market is entering the 6th month of correction from the Jan. 29 peak of 9,058, which in the recent past three corrections lasted on the average by 7 months. Other key economic releases this week are the latest FOMC minutes and US jobs data on July 5 (US time).

Market Review. PSEi continued to buck regional trend, rising 34.3 points (+0.5% day-on-day, d/d) on Monday to close at 7,227.9. Last week, it rebounded by 130.5 points (+1.8% week-on-week, w/w) to end at 7,193.7 buoyed by second quarter window dressing after PSEi touched a 17-month low of 6,986.9 on June 25 and ahead of Pres. Trump’s tariff implementation this month.

- PSEi recorded the 5th straight month of decline in June, down 4% month-on-month (m/m). Year-to-date (YTD), it was one of the world’s underperformers, down 15.9% amidst 22 weeks of consecutive net foreign outflows totaling P70.3bn. From its peak on Jan. 29, the market fell 20.6%, putting it in a bear market.

- Last week, net foreign selling was the lowest since the start of the correction at P415mn. YTD, net foreign selling totaled P65.8bn.

- W/w, PSEi bucked global trends as all the markets that we follow were down led by Thailand (-2.4%), US Nasdaq (-2.4%) and Germany (-2.2%). YTD, PSEi led the underperformers, followed by China (-13.9%) and Thailand (-9%).

- PHP closed on Friday at P53.32/%, down 0.1% w/w and 6.4% YTD amid heightened concerns on the country’s deteriorating external position.

- Last week, foreign investors bought MER, SMPH, TEL, URC and BDO for an aggregate amount of P1.5bn, and sold JFC, BPI, AGI, ICT and MBT totaling P1.2bn. YTD, only MER, TEL and PGOLD recorded net inflows amounting to P3.3bn, while SM, ALI, BDO, AC and JGS recorded substantial net outflows of P32.1bn.

Economic News

Market expects June inflation to register at 4.7% y/y, slightly faster than May’s 4.6%, but at the midpoint of BSP’s guidance of 4.3-5.1% due to higher food and oil prices, coupled with weak PHP. This implies a m/m consumer price increase of 0.1%. Oil prices reached a 3 1/2 year high on June 29 to $74.15/barrel amid fears of supply disruptions while PHP weakened by an average of 1.6% m/m due to concerns on deteriorating current account deficit which the BSP is now expecting to reach $3.1bn in 2018 from 2017’s $2.5bn. We (house view) expect inflation to peak in June at 4.7% y/y and should be in a downward trend until at least in the H1 2019 as the impact of TRAIN and rising oil prices subside. Bangko Sentral ng Pilipinas (BSP) disclosed that money supply in May rose 14.3% y/y to P11trn, slightly faster than previous month’s 14.2%. Meanwhile, bank lending rose by 19.4% y/y (net of RRPs) from April’s 19.9% driven by robust expansion in corporate and consumer lending. Loans for productive activities sustained its growth of 19.3% y/y from April’s 19.6% led by construction (+32.9%), wholesale and retail trade (+23.4%) and real estate (+15.7%). Likewise, consumption lending expanded at a strong pace of 18.4% y/y, buoyed by above 20% growth in credit card (+21.1%) and motor vehicles (+22%).

Corporate News

Jollibee Foods Corporation (JFC) targets to acquire a Mexican food chain in the US, possibly within the year, as part of its goal to become one of the largest fast food chains in the world as it aims to achieve a 50/50 local and foreign business as early as 2023, with overseas business comprising 30% of its business now. JFC is set to open 500 new stores this year (250-300 will be located in the PH) and get into Malaysia, Indonesia and United Kingdom. JFC closed on Monday at P260 a piece, +2.8% YTD.

Read full article here.

Related Articles

Insights and Announcements

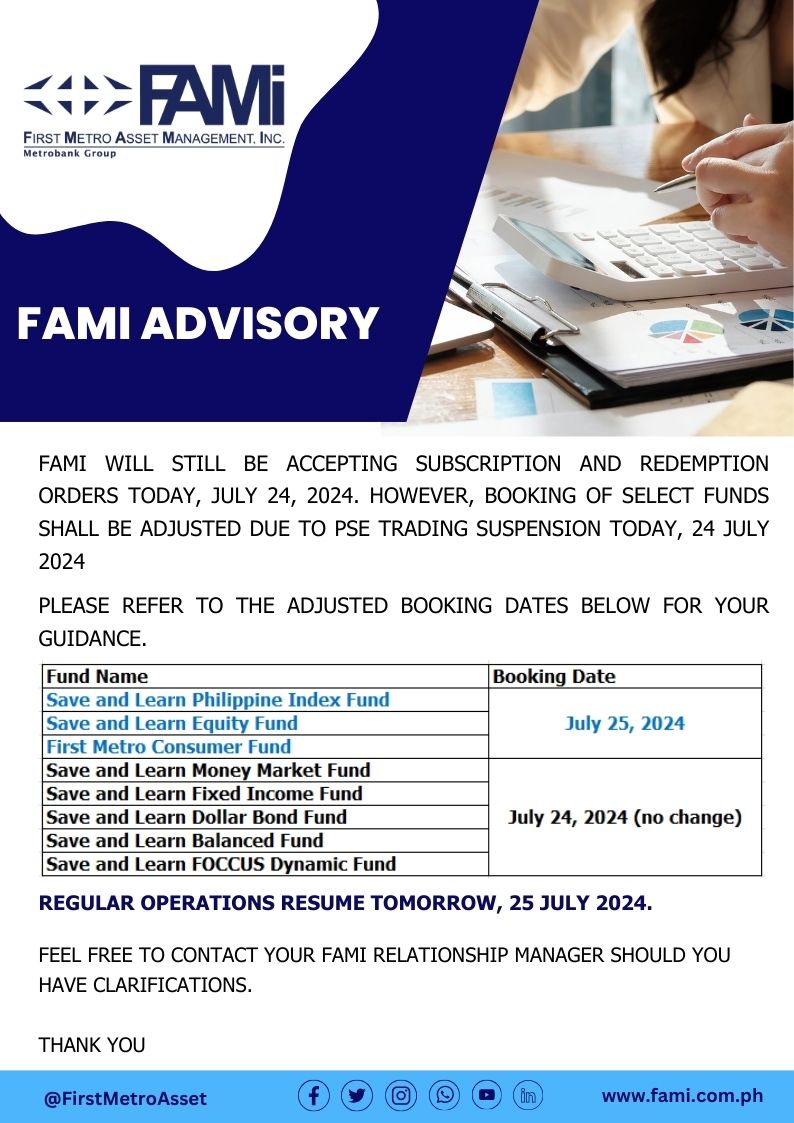

FAMI BOOKING ADVISORY