Angelo Silva

Jun 19, 2018

3 mins

Equities Summary and Outlook

Outlook. We expect the PSEi to trade between 7,300 - 7,600 this week as the market digests the impact of escalating trade war between US & China and sustained PHP weakness. Key economic event this week is the Monetary Board (MB) meeting on June 20 where the market expects policy rates to be kept steady at 3.25% due to easing inflationary pressure.

Market Review. PSEi dropped by 115.4 points today to 7,414.1 (-1.5% from Friday’s closing) as global markets digest the brewing trade war. Last week, PSEi closed lower at 7,529.5 (-211 points or -2.7% week-on-week, w/w) on Friday, as the PHP reached a 12-year low of P53.28/$ on Friday following Fed’s decision to raise policy rates by another 25 bps. The local bellwether was down 12% year-to-date (YTD) and 17% from its all-time high of 9,058 on Jan. 29 on the back of massive net foreign selling in the last 20 weeks totaling P63.3bn. Last week, net foreign selling accelerated to a 12-week high of $4bn.

- Markets were mixed YTD. Top gainers were US Nasdaq (+12.2%), India (+4.6%) and Taiwan (+4.2%), while top underperformers were the Philippines (-12%), China (-8.6%) and Thailand (-2.8%).

- PHP remained the weakest currency in Asia, down 6.3% YTD and 1.1% w/w due to wider trade deficit ($12.2bn YTD April, +59% year-on-year, y/y) and higher US interest rates.

- MER, SECB and PGOLD were the most bought stocks last week with net inflows of P515mn, while MBT, SMPH, ALI, AC and SM were the most sold stocks with net outflows of P2.7bn. YTD, foreign investors purchased MER, TEL and PGOLD with net inflows of P2.8bn, and sold SM, ALI, BDO, AC and JGS for a net aggregate amount of P30bn.

Economic News

Bangko Sentral ng Pilipinas (BSP) reported that OFW cash remittances recovered in April, up 12.7% y/y to $2.3bn, following a 9.8% y/y decline in March. This was the fastest pace since Nov. 2016’s 18.5% growth. US, Canada and Singapore were the biggest sources of growth, contributing 4.2 percentage points, 1.9 percentage points and 1 percentage point, respectively. Meanwhile, personal remittances grew 12.9% y/y to $2.6bn. Cumulatively, cash remittances expanded by 3.5% y/y to $9.4bn, while personal remittances rose 4% y/y to $10.4bn, in line with our (house view) full-year 2018 forecast of 2-4%. BSP also reported that current account (CA) deficit in Q1 2018 tallied at $208mn, lower than $3.3bn in Q4 2017 and $860mn in the same period last year. Higher trade-in-goods deficit ($10.4bn from $9.7bn in Q1 2017) was partially offset by higher net receipts from trade-in-services ($3bn from $1.8bn in Q1 2017) with export revenues from BPO growing by 7.5% y/y to $5.5bn, and net primary and secondary income ($7.2bn from $7.1bn in Q1 2017) which mostly came from OF remittances. BSP revised its BOP account forecasts for 2018. Projected current account deficit was raised to $3.1bn (~0.9% of GDP) from the original forecast of $700mn deficit due to expectation of wider trade deficit from higher imports. Goods imports growth was slightly raised to 11% from 10%, and exports to 10% from 9%. Projected net FDIs was $9.3bn, slightly lower than 2017’s actual net inflows of $10bn. Overall BOP deficit was increased to $1.5bn (~0.4% of GDP) from the original forecast of $1bn.

Corporate News

Wilcon Depot (WLCON) guided for mid-teens growth in net income and mid- to high-teens growth in sales for 2018. The company aimed to achieve a gross profit margin of 31% this year, a tad higher than the 30% margin in 2017 by increasing the share of in-house brands to total sales from 44.5% to 46%, and same store sales growth of 5%, slightly lower than the 6% growth in the past two years. WLCON ended today at P11.56/share, up 40% YTD.

Read full article here.

Related Articles

Insights and Announcements

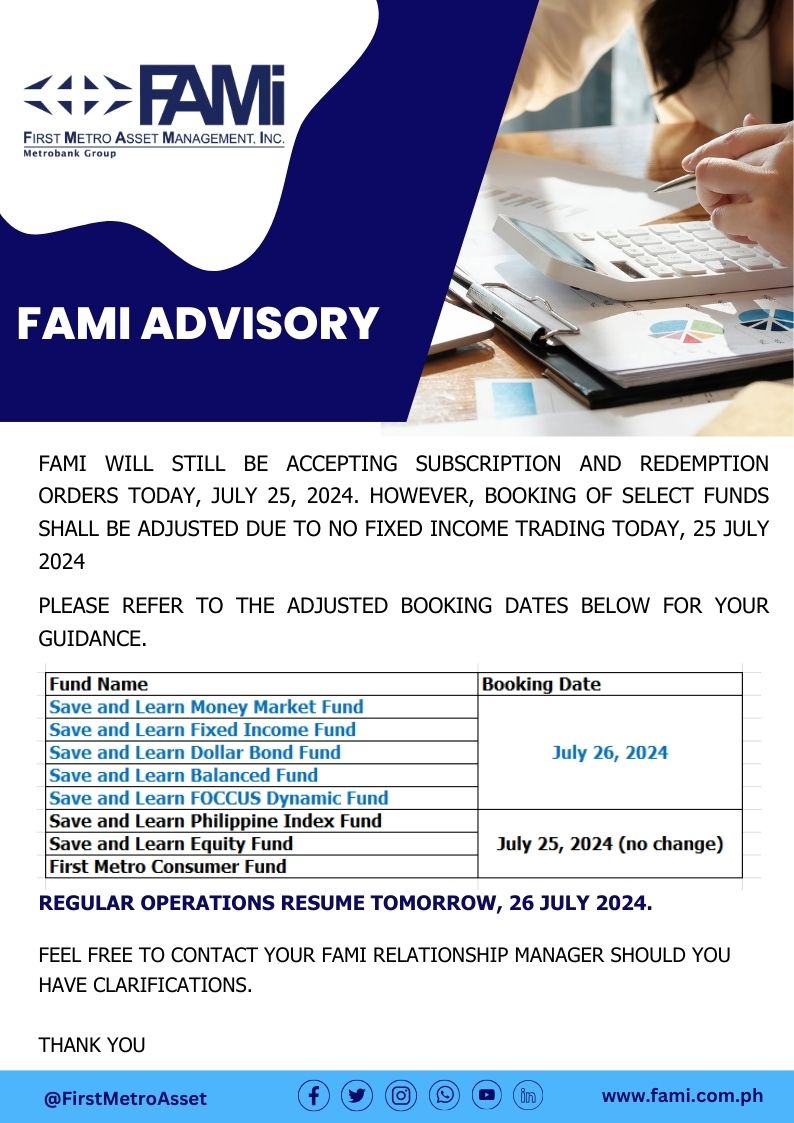

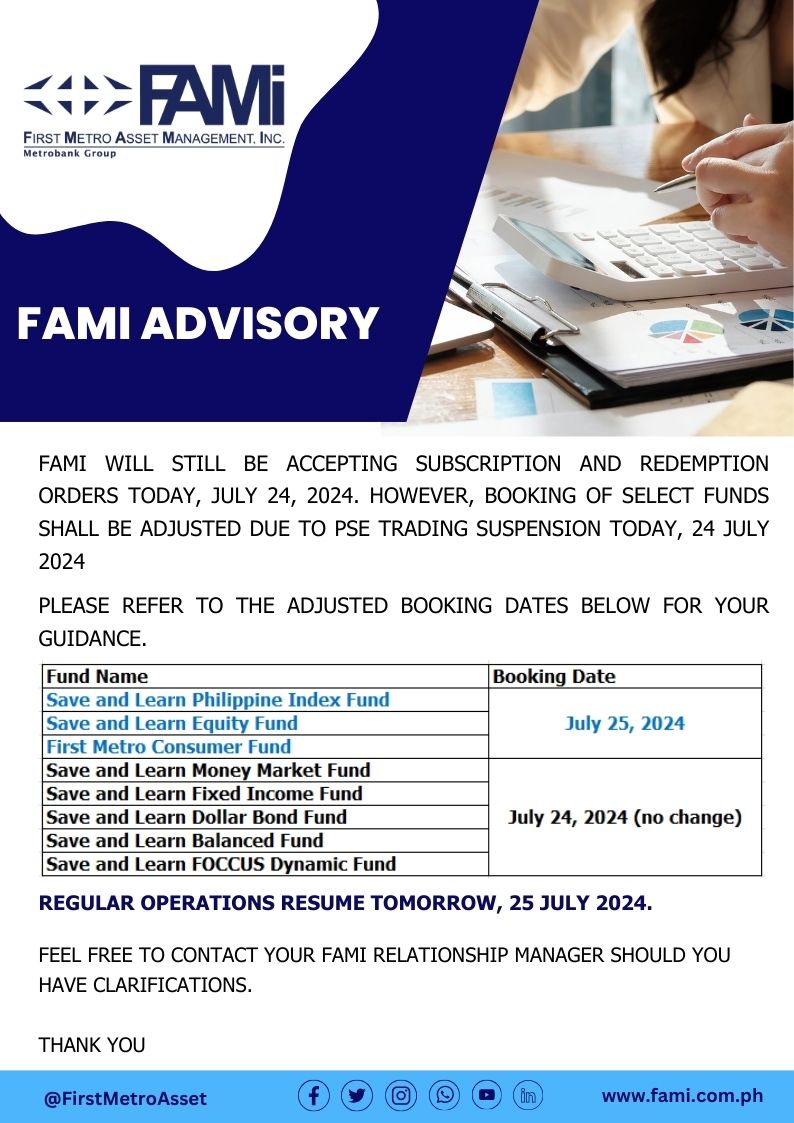

FAMI BOOKING ADVISORY

Insights and Announcements

FAMI BOOKING ADVISORY