Angelo Silva

Jun 14, 2018

4 mins

Equities Summary and Outlook

Outlook. We expect the market to continue trading within 7,500-7,800 amidst shortened trading week due to observance of holidays. Additionally, investors remain on the sidelines waiting for signals from the upcoming US Federal policy meeting. The European Central Bank and Bank of Japan are also scheduled to meet this week. There’s downward bias as the peso breached P53 for the first time in 12 years. Key events to monitor are US FOMC rate decision on Thursday and BSP Overnight rate on June 21.

Market Review. The market closed 110.48 points higher or 1.45% week-on-week (w/w) to 7,740.74 on Friday triggered by better than expected inflation for May which clocked in at 4.6%, less than consensus’ expectation of 4.9%. From its peak of 9,058 on Jan. 29, the local bellwether was down by 14.5%.

- Year-to-date (YTD), the PSEi was down 9.6%, worst performing market in the region following China’s 7.3% decline. The top performing markets were Taiwan (4.8%), India (4.5%) and Hong Kong (3.5%). W/w, Asian markets mostly ended in the green with only China ending in red at -0.3%.

- Foreigners were still net sellers, now at its 19th consecutive week totalling P55.1bn ytd. Last week, net outflows was at P2.1bn, the least weekly amount sold in a month.

- Trading volume continued to be thin at P5.8bn last week and thinner at P4.0bn last Monday. Today, total value traded was higher at P7.1bn albeit still below the P7.7bn average.

- PHP weakened on Friday at P52.70/$ (-0.3% w/w) but breached the P53 level today at P53.23. YTD, it is down by 6.6%.

- Foreigners’ top buys were MER, SMPH, MPI, GLO and PGOLD for an aggregate amount of P696.4bn. Meanwhile, foreigners sold MBT, LTG, URC, SCC and GTCAP amounting to P1.1bn.

Economic Summary

The country’s gross international reserves (GIR) level as of end-May 2018 declined to $78.9bn, 0.81% lower than the previous month’s GIR of US$79.6bn and 3.9% lower than the $82.2bn recorded in May 2017. Additional details below:

- This GIR level is the lowest since November 2017 when it touched $78.7bn. Import cover during that period was at 9.9x.

- The value of the central bank’s foreign investments dropped to $63.7bn in May from $64.5bn in April.

- End-May 2018 GIR level is equivalent to 7.7x months of imports of goods and payments of services and primary income.

- This is also enough to cover 5.4x the country’s short-term external debt based on original maturity and 3.9x based on residual maturity.

- Meanwhile, net international reserves (NIR) (difference between the BSP’s GIR and total short-term liabilities), was lower at $78.95bn as of May 2018 from April’s $79.6bn.

Corporate News

Metro Pacific Investments Corp’s (MPI) tollway arm, Metro Pacific Tollways Corp., will raise as much as P23.5bn to fund the Cavite-Laguna (CALAx) project. According to MPTC President & CEO Rodrigo Franco, this amount will be borrowed from banks by July. Meanwhile, another unit, MetroPac Water Investment Corp, finished the acquisition of a 49% stake in Tuan Loc Water Resources Investment Joint Stock Company, one of the largest water companies in Vietnam. The unit purchased 37.926m shares equal to P2bn.

Read full article here.

Related Articles

Insights and Announcements

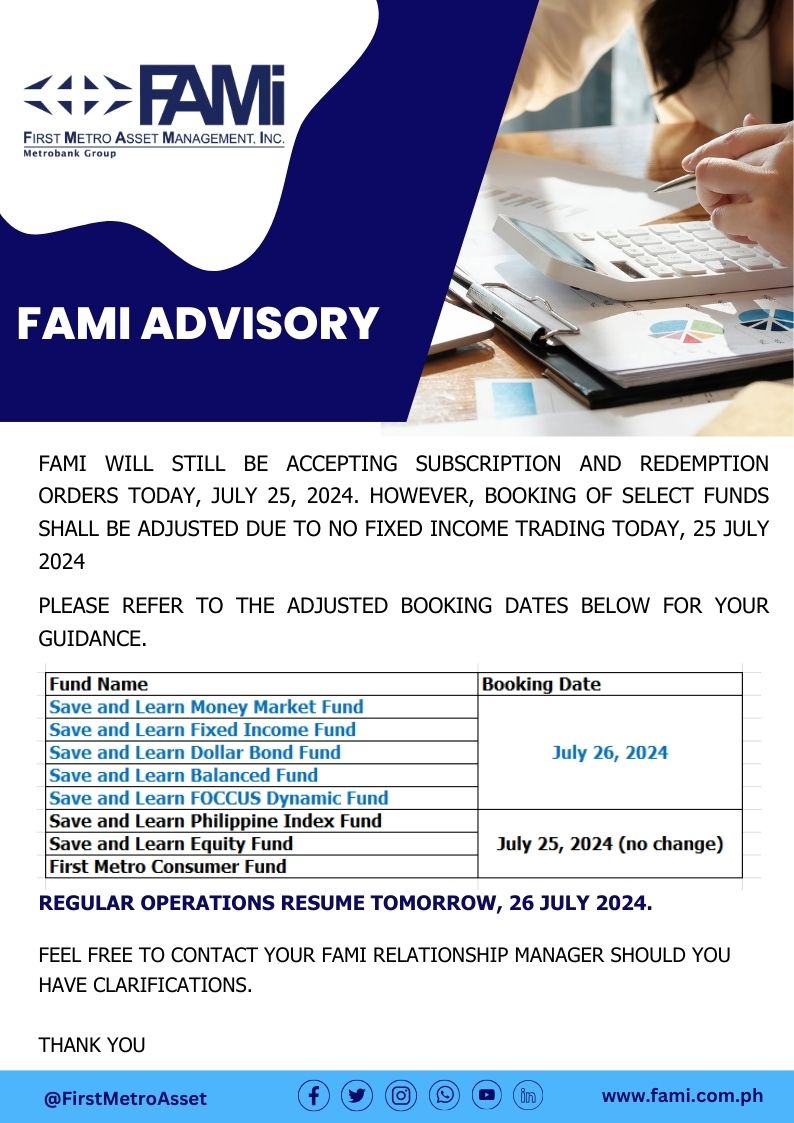

FAMI BOOKING ADVISORY