Angelo Silva

Aug 07, 2019

8 mins

Equities Outlook

Outlook. Expect the market to follow the correction seen in the global markets. The PSEi is expected to trade somewhere around the 7,700 – 7,900 support, dragged by global headwinds, MSCI rebalancing, and local corporate earnings. Trade war escalation will remain the theme in the global market for the week, although we may find some comfort from a stronger case of policy rate cut in the next FOMC meeting in September. For his part, BSP governor Diokno announced that the BSP is poised to cut policy rates by 50bps before the year ends, with some already expecting the first 25bps to be announced as early as Thursday’s meeting. This is on top of the 25bps rate cut in May and 200bps reduction in reserve requirement ratio which were applied in three phases ending in July. This announcement was a response to the continued sluggish growth in money supply (M3 grew 6.4%), expected tepid GDP growth in 2Q19 (consensus forecast at 6%), and suppressed inflation in the second half (expected to average 2.6% in 2019). We also expect some profit taking ahead of MSCI semiannual index review, which is expected to see Philippines’ weight in the index reduced further in favor of China A-shares.

So far, the strong start of the earnings season was dampened by new disclosures from other index members. Despite BPI validating strong growth from the financial sector in 1H19 (net income up 24.6%), we saw earnings decline from AEV, AP, and RRHI last week while GLO was unable to sustain strong growth in 2Q19 despite strong revenues as expenses, particularly depreciation, picked up. This week, we observed some pockets of weakness from ALI which, despite the 12% net income growth in 1H19, saw residential revenue decline 11% in 1H19 and pre-sales contract 6% in 2Q19 (flat 1H19) attributed to ALP and Alveo projects’ stronger than expected take-up eating up inventory. ALI already rallied 26% year-to-date and may see some profit taking based on news. JFC also saw net income declined by 50.2% in 2Q19 and 1H19 by 34.4% due to Red Ribbon’s supply disruptions from transferring to new plant and Smashburger’s continued struggles. Recovery is not expected until 2020 for these two brands but expect income to remain subdued as the company completes its acquisition of CBTL which will only be net income accretive 12-18months after completion of the deal. For the rest of the week, index members SM, SECB, SMC, TEL, and RLC will hold briefing regarding 1H19. BDO and SMPH already points to SM’s resilience in 1H19. We expect SECB to improve this quarter, following the strength of the overall sector led by the top three banks. RLC may correct from its current price after recently touching new 52-week highs despite strong 2Q19 results and 2H19 guidance as the market digests the new property dividend from Altus San Nicolas Corp and its implication to RLC’s NAV. SMC may still be dragged by PCOR as oil prices continue to slump and TEL, although expected to post strong topline growth, remain challenged in as costs are expected to rise further and CAPEx will remain elevated as it prepares for the entry of the third telco.Market Review. The main bourse ended the week 0.7% lower, closing at 8,129.9. As cautioned, the market dipped below the 8,000 but held on to the initial support of 8,100 last week. The index fell by as much as 208pts last Thursday, reaching a low of 7,975, on news of escalating trade wars and less dovish Fed, before reversing and closing 130pts higher from that low. AEV and AP were among the top losers, down 6.1% and 5.0% respectively, due to weak earnings. AEV’s core earnings were down 16% in 1H19 to Php10.6bn, dragged mainly by AP which saw net income contract by 19% to Php8.5bn, both disappointing consensus estimates. GLO was also in last week’s top losers, down 5.4% for the week, as net income in 2Q19 fell 2%, failing to sustain the 40% growth in 1Q19. First half 2019 core income was still up 18% and managed to stay in line with consensus estimates. Daily value turnover averaged Php6.3bn while net foreign buying was registered at Php292mn for the week, led by investments in SM, JFC, BPI, MEG, and BDO.

Regional Markets. Global markets were down last week after Powell signalled that the 25bps cut implemented last week was not yet the start of policy easing, sparking speculation that the Fed may be less dovish than initially anticipated. The announcement came after Trump announced 10% tariff on US$300bn Chinese imports effective Sept 1 as negotiators failed to make progress in the recent US-China trade talks. US markets, represented by Dow Jones and S&P 500, saw these news as opportunity to lock in gains from recent highs selling the market down 2.6% and 3.1% respectively. Shanghai Composite Index was down 2.6% while Hang Seng fell 5.2% lower for the week as continued protests exacerbated global jitters felt by the global markets.

Currencies. Asian currencies continued to decline last week, with the Philippine peso finally joining the fall as dollar continued to strengthen on strong US data and less dovish Fed. The Dollar spot was up by as much as 0.5% last week, before ending the week up by 0.2%. The Philippine peso was down 0.8% last week, closing at Php51.44/USD. Indonesian Rupiah fell 1.3% while South Korean Won was down 1.1%. Malaysian Ringgit and Chinese Yuan were also down 0.9% while Japanese Yen, seen as safe haven, rallied 1.9%.

Economic News

Loan growth slowed down to 10.5% in June from 11.9% in May, dragged by loans for production activities which slowed down to 9.8% in June from 11.5% in the previous month. Consumer lending continued to be strong, in fact it accelerated to 15.3% from 14.6% in May. Money supply, measured by M3, grew 6.4% in June 2019 same with May 2019. BSP expects July inflation to settle between 2.0% – 2.8% pulled down by lower rice, LPG prices, peso appreciation, and downward adjustment in electricity rates. Analysts’ forecast for July inflation ranges between 2.2% - 2.6%, lower than 2.7% in June 2019.

Corporate News

BPI net income was up 24.6% year-on-year to Php13.7bn, in line with consensus. Net interest income was up 24.1%, driven by 10.8% loan growth and net interest margins (NIM) expansion of 38bps. Thanks to 103bps improvement in asset yields, outpacing higher cost of funds. Non-interest income grew 21.5% to Php13.5bn, attributed to increases in securities trading gains and fee-based income. Operating expense in 1H19 grew 14.4% which brought cost-to-income ratio down to 52.9% from 57% in the same period last year. NPL ratio was flat at 1.86% vs end 2018. BPI remain well capitalized with CET-1 ratio of 15.55% and Capital Adequacy Ratio of 16.44%.

RRHI core net income fell 24% dragged mainly by PFRS 16 adjustments. Pre-PFRS, net income grew 1% in 2Q19, an improvement from the 16% drop in 1Q19. Rustan’s posted a positive Php42mn EBIT in 1H19, a reversal from negative Php171mn EBIT in 1Q19, driven by gross profit gains brought by alignment of trading terms between Robinsons and Rustan’s and higher distribution center and listing fees to its suppliers. Operating margins also improved due to lower overhead count and alignment of depreciation policy. Rustan’s is expected to be profitable by end of 2019. RRHI same store sales growth (SSSG) slowed down to 3.7% in 2Q19 coming from 4.1% in 1Q19, bringing 1H19 SSSG to 3.9%. Drugstore posted the strongest SSSG at 11.2% in 1H19 while other segments slowed down with the Department Store seeing same store sales declined 1.2% year-on-year (y/y) in 1H19 pulled by -3.5% SSSG in 1Q19 due to renovation of top stores and competition although second quarter has already recovered posting 0.7% SSSG y/y. AEV 1H19 net income fell 16% to Php8.9bn, dragged mainly by AP which saw core net income drop 19% to Php8.5bn for the same period. Other segments also struggled. Adjusted for contribution to AEV, AP fell to Php6.5bn, down 19% due to over-contracting, outtages, and high spot prices in WESM. Pilmico fell 17% to Php552mn and AboitizLand down 79% to Php60mn. Unionbank grew saw 52% growth in 2Q19, bringing 1H19 contribution to Php2.37bn, up 3%. Thanks to higher NIMS, fee income, and trading gains. Republic Cement grew 5.66x in 1H19 to Php249mn, driven by better prices and lower production costs. Republic Cement also saw improved volume from private sectors, helping its performance. MPI core net income came in flat at Php8.67bn, ahead of consensus. Toll road revenue and EBITDA both grew 20%, driven by partial tariff resolutions at NLEx and SCTEx, offsetting jump in interest expense. In effect, toll road income contribution grew 6% to Php2.4bn. Hospitals grew 18% to Php400mn, the power business grew 4% while Maynilad saw 9% growth in 1H19. Management is pushing to complete its divestment from its hospital business before the year ends. Proceeds will be used for CAPEx and debt management. Read full article here.

Related Articles

Insights and Announcements

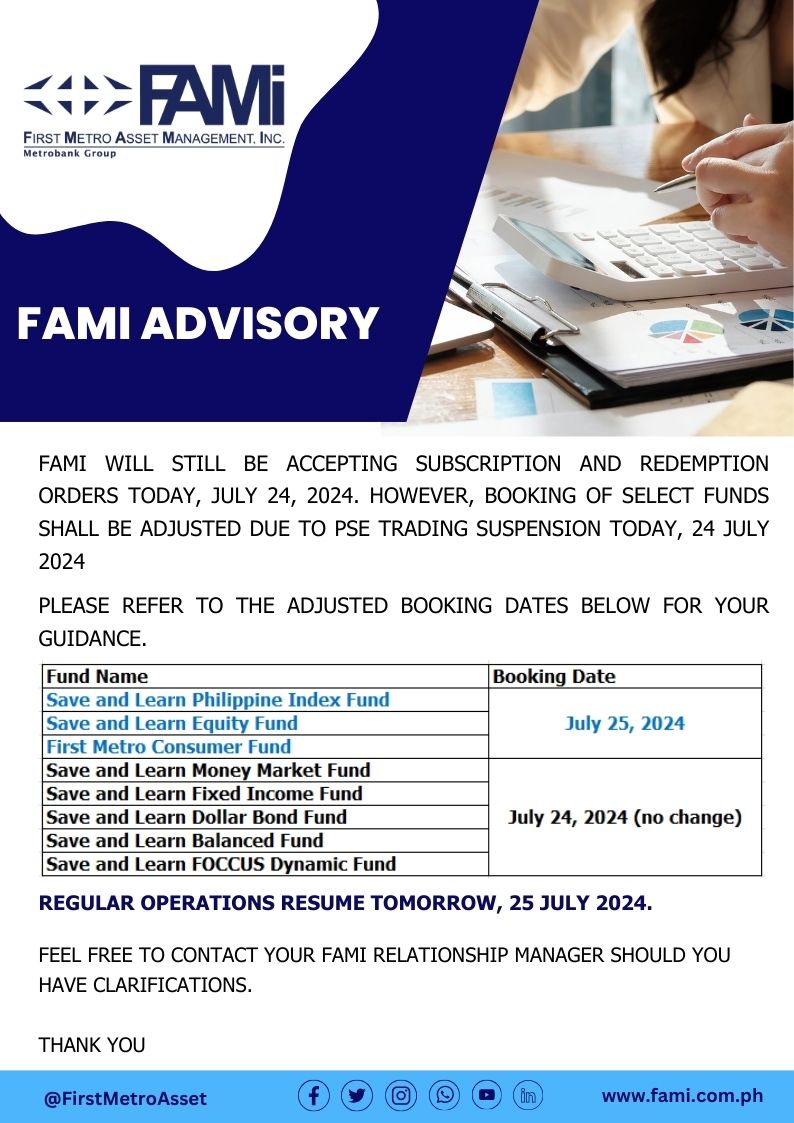

FAMI BOOKING ADVISORY

Insights and Announcements

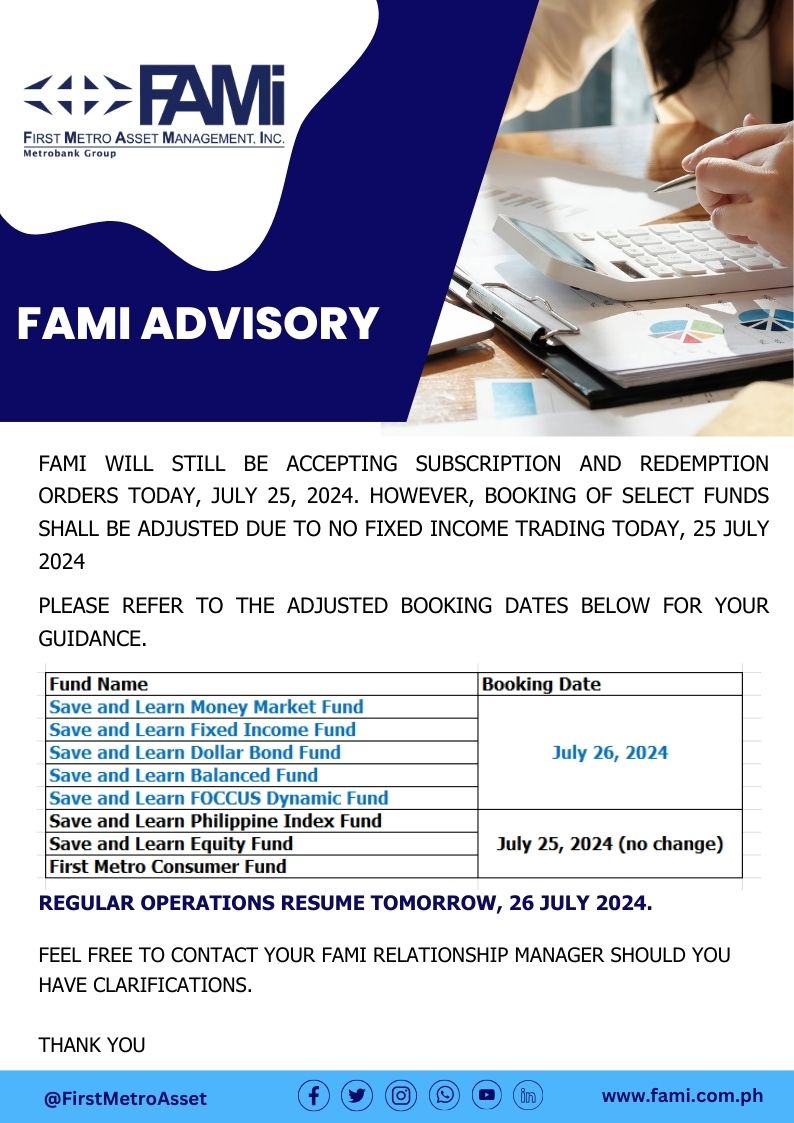

FAMI BOOKING ADVISORY