Angelo Silva

Apr 16, 2019

5 mins

Equities Outlook

Outlook. We expect the PSEi to consolidate within the 7,800 – 8,000 range after the index failed to hold above 8,000 due to the 2019 government budget impasse, global growth slowdown reflected in the recent cuts by the IMF and ADB for the global growth outlook and the Philippines to 6.4% from 6.5% for the former and 6.4% from 6.7% from the latter. The market will remain cautious and quick to take profits specifically on news that the 2019 government budget was already signed by the President and also on positive global news about developments in the US-China trade dispute which President Trump described as making good progress. The latter tended to underpin short-lived rallies in Asian emerging markets in the past weeks. The downside risk would be in terms of GDP growth in the first quarter given the adverse impacts of the budget delay on the fiscal stimulus/government spending and also of the El Nino on agricultural output. Thus, the market may weaken in May once the 1Q2019 GDP growth is out (late May), widely expected to be slower than last year’s comparable 6.5%. Simultaneously, investors attention will also focus on the first quarter corporate earnings which may mirror in part the weakness in first quarter GDP as well.

The upside, however, would be in the BSP’s much awaited action on the triple R, a cut that is bet at 1% down to 17% and the BSP language surrounding the said cut, if it provides clues as to how many more cuts are likely this year. Will the BSP sound more dovish? That will be positive for the market as it signals more liquidity easing. The biggest potential jolt to the market in May could be the MSCI global index rebalancing that includes China mainland shares raised to 10% of the index, coming from 5%. This will cause displacements in the index weights of emerging markets that include the Philippines in the MSCI global indices as well as in the other global indices such as FTSE and S&P Global indices. The estimated Philippine market equities outflow upon the rebalancing implementation ranges from $600m to $1.5bn, the former from CLSA and the latter from Macquarie, respectively.Market Review. The PSEi managed to end the week in the green, closing at 7,880.8, up 0.1% w/w. The index rallied to 8,008 on Wednesday before succumbing to profit-taking ahead of the shortened holy week.

Market Flows. The week ended with Php2.9bn net foreign buying, bringing ytd net buying to Php38.5bn. Market participation was dominated by foreigners at 59% of the market activity. Top recipients were ALI (Php403.7mn), URC (Php384.2mn), and SM (Php298.9mn).

Regional Markets. The US market managed to sustain its 2019 rally thanks to positive 1Q19 earnings results from banks, kicking off the earnings season. JP Morgan Chase beat analysts’ EPS estimates by 12.7% posting earnings per share of US$2.65 vs consensus, while Wells Fargo posted earnings per share beat expectations by 10%. The EU markets meanwhile were hampered as Brexit deals were again stalled.

Currencies. The peso was up 0.7% for the week thanks to continued foreign portfolio investment. Foreigners were net buyers for the fifth straight week, last week. Peso also strengthened thanks to narrower-than-expected trade deficit of US$2.8bn vs Bloomberg consensus’ US$3.4bn, owing it to a slower import growth of 2.6% to US$8.0bn.

Economic News

Trade deficit in the first two months widened by 16.4% y/y to US$6.7bn. February exports fell for the third straight month to US$5.2bn y/y while imports grew 2.6% to US$8.0bn. Trade deficit was lower than consensus estimate of US$3.4bn as imports’ expanded slower than the 6% growth the consensus anticipated.

Foreign Direct investment contracted 38% in January as equity investment fell 94.3% to US$31mn, as withdrawals of US$229mn outpaced the US$184mn in placement. The US$76mn in reinvestment of earnings kept equity investment positive. Investment in debt instruments carried the load, bringing US$577mn of inflow, up 31%.Corporate News

MEG, AGI, and PGOLD completed the PSE index’s corporate earnings last week. Weighted core net income was up 8.7% while growth of sum (summation of net income of 30 index stocks) was up 7%.

MEG reported 16.8% net income growth, slightly ahead of expectations. Revenues grew 14.6% as all segment posted double digit led by leasing business which grew 20.6% y/y. Real estate sales and hotel business saw 11.5% and 13.7% growth respectively. The faster growth of high margin leasing business saw consolidated margin expand by 170bps. While MEG saw impressive growth, other business segment of Alliance Global Inc (AGI) dragged, leaving AGI’s FY18 net income flat y/y to Php15.1bn as its consumer businesses saw challenging year brought by higher inflation and weaker peso both contributing to higher COGS. PGOLD core net income was up by only 5% to Php6.15bn, missing estimates. Including the Php363mn gain from Lawson divestment, income was up 12% to Php6.5bn. Management cited lower listing fees and display allowances from suppliers as manufacturers cut back in promotional expenses in to offset cost pressures brought by elevated inflation and steep peso depreciation last year. Read full article here.

Related Articles

Insights and Announcements

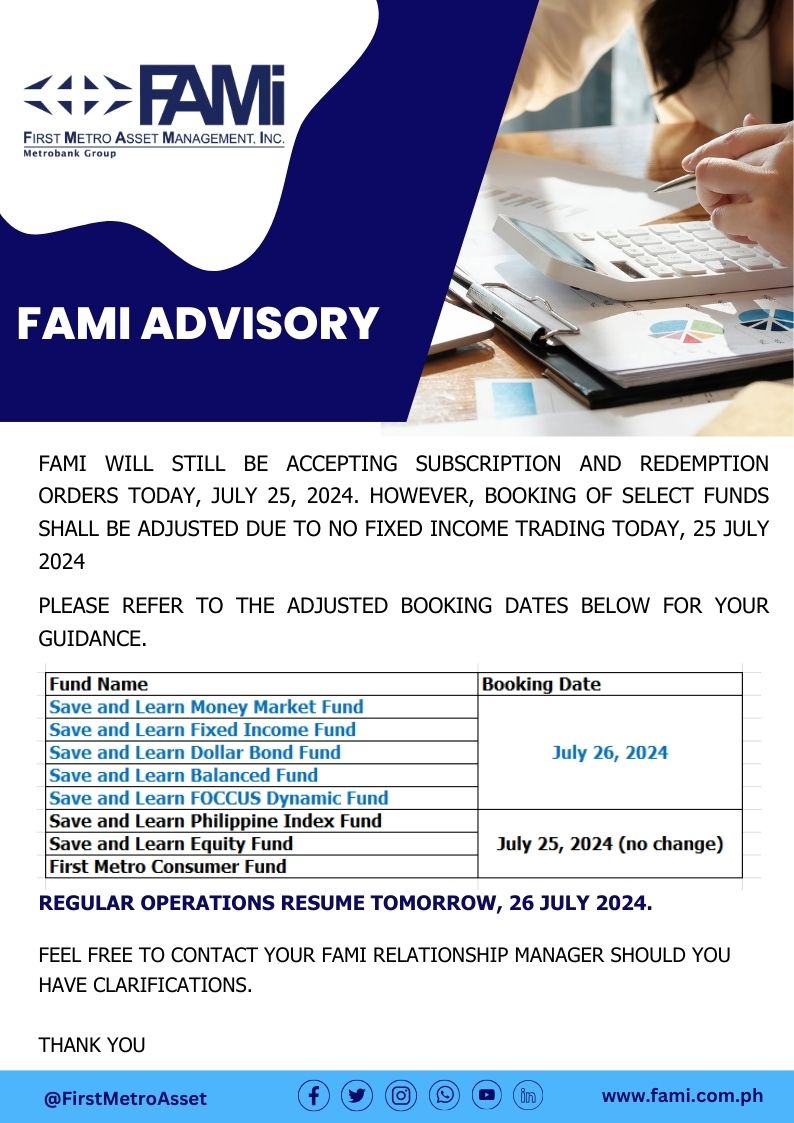

FAMI BOOKING ADVISORY

Insights and Announcements

FACTORS AND FORCES OF INVESMENT WEBINAR February 4, 2023