Written By

Angelo Silva

Angelo Silva

Published on

Aug 17, 2010

Aug 17, 2010

Reading time

4 mins

4 mins

Share this article

Related Articles

Insights and Announcements

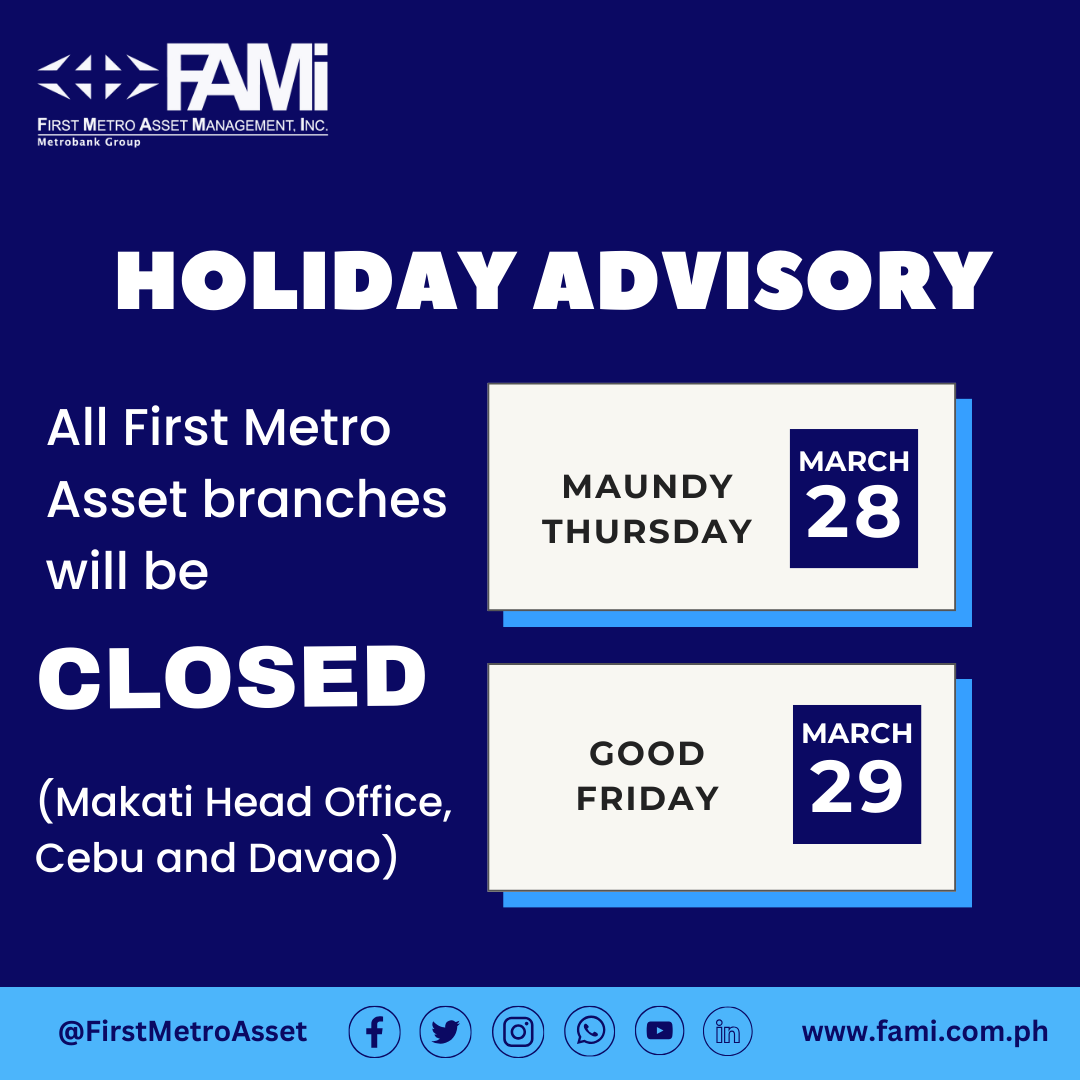

Holiday Schedule - Holy Week