Angelo Silva

Mar 07, 2019

4 mins

Inflation Downtrend Raise Odds of Rate Cut

Outlook. Local inflation last February was a nice surprise, hitting 3.8% which was lower than consensus expectation (4.0%) and January’s 4.4%, mainly driven by food and non-alcoholic beverages, alcoholic beverages and tobacco, and transport. This dislodged the peso from strength from almost a year-low of Php51.710 to back to above Php52 on hopes of lower interest rates. This also boosted the odds for a reserve requirement cut. Meanwhile, the Bangko Sentral (BSP) expects inflation to trend lower for the rest of Duterte’s term, which could apply downward pressure on the yield curve. The market fully priced in the Php114bn auction of 5-yr retail treasury bond (RTB) last week as the yield curve ended the week relatively unchanged. The bond was offered at 6.25%, at the higher end of the expected range by the market. The RTB will be available to the public from February 26 to March 8.

In the US, growth domestic product (GDP) grew by an annualized rate of 2.6% in the fourth quarter, faster than the expected 2.2% growth but slower than 3.4% in the third quarter, driven by a 2.8% growth in consumption. However, construction spending declined by 0.6% in December from a 0.8% increase in November and 1.6% YoY. For the entire year, construction rose by 4.1%, the weakest reading since 2011, which economists expect may lead to a downward revision of the fourth quarter GDP number by the end of March to 2.5%. President Duterte named former Budget Secretary Diokno as new BSP Governer after the death of former Governor Espenilla last week.Market review. The local benchmark yield curve was flat, down by just 0.3bps on average week-on-week (WoW) amid the RTB issuance. The spread between the local 10-yr local benchmark and the 10-yr US Treasury (UST) narrowed further to 356bps from 363bps in the week prior as the former rose by 4bps to 6.32% while the latter likewise was up by 11bps to 2.65%. Year-to-date, the yield curve and the 10-yr were both down by an average of 75bps. Yields of ROPs were down flat on average while US Treasuries rose by 6bps.

Average total daily flat week-on-week (WoW) to Php9.9bn. The liquid yield curve rose by an average of 1bp WoW as the front-end (364-day T-bill) fell by 4bps to 6.06%, the belly (FXTN 10-63: 9.5yrs) up by 3.6bps to 6.32%, while the tail (R25-01: 20.5yr) fell by 6bps to 6.73%. Secondary trading average volume was flat at Php9.9bn as the 34% drop in T-bill trading to Php2.7bn was offset by the 21% increase in T-bond trading to Php10bn. Results of the latest Php15bn were mixed; bids for the 91-day and 364-day T-bills were rejected, while the 182-day was partially awarded at 5.975%, 3bps lower than the previous auction. The auction raised only Php3.9bn of the Php20bn offered.

Emerging Markets’ (EM) 10-year flat (WoW). Yields of EM bonds we follow were flat WoW ahead of a bevy of EM central bank meetings this week, though none of them are expected to cut rates any time soon amid low inflation across different EM countries. Chile (10-year yield -34bps), Indonesia (-9bps), and Mexico (-8bps) outperformed, while Poland (10-year yield +21bps), Hungary (+9bps), and China (+6bps) underperformed.

USTs up 6bps WoW. US Treasuries rose by 6bps WoW on average as the 10-yr UST likewise increased by 11bps to 2.76% as the market bought the news of a faster-than-expected GDP growth in the fourth quarter. There is also optimism on the trade front that an agreement is close as Trump cited “substantial progress” on a slew of issues, especially regarding Chinese purchases of US agricultural products and services. Bloomberg reported that U.S. officials were drafting a deal that Trump and Xi Jinping could sign as early as mid-March.

Read full article here.

Related Articles

Insights and Announcements

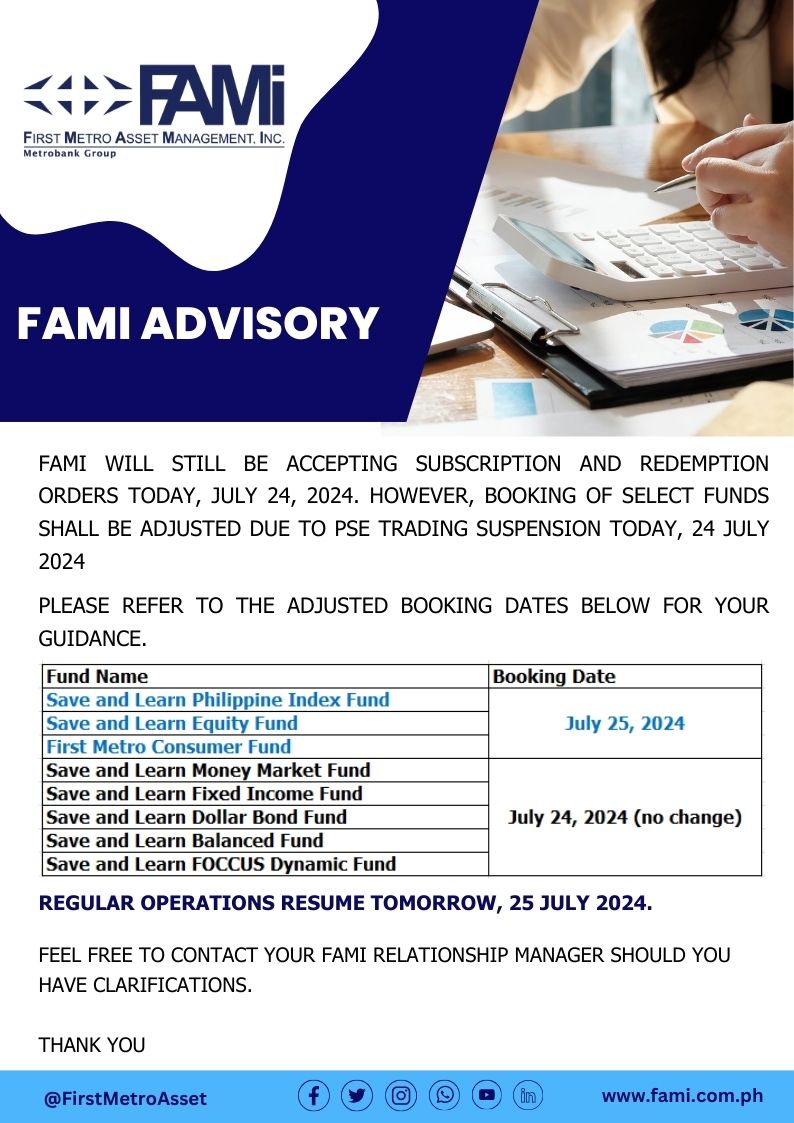

FAMI BOOKING ADVISORY