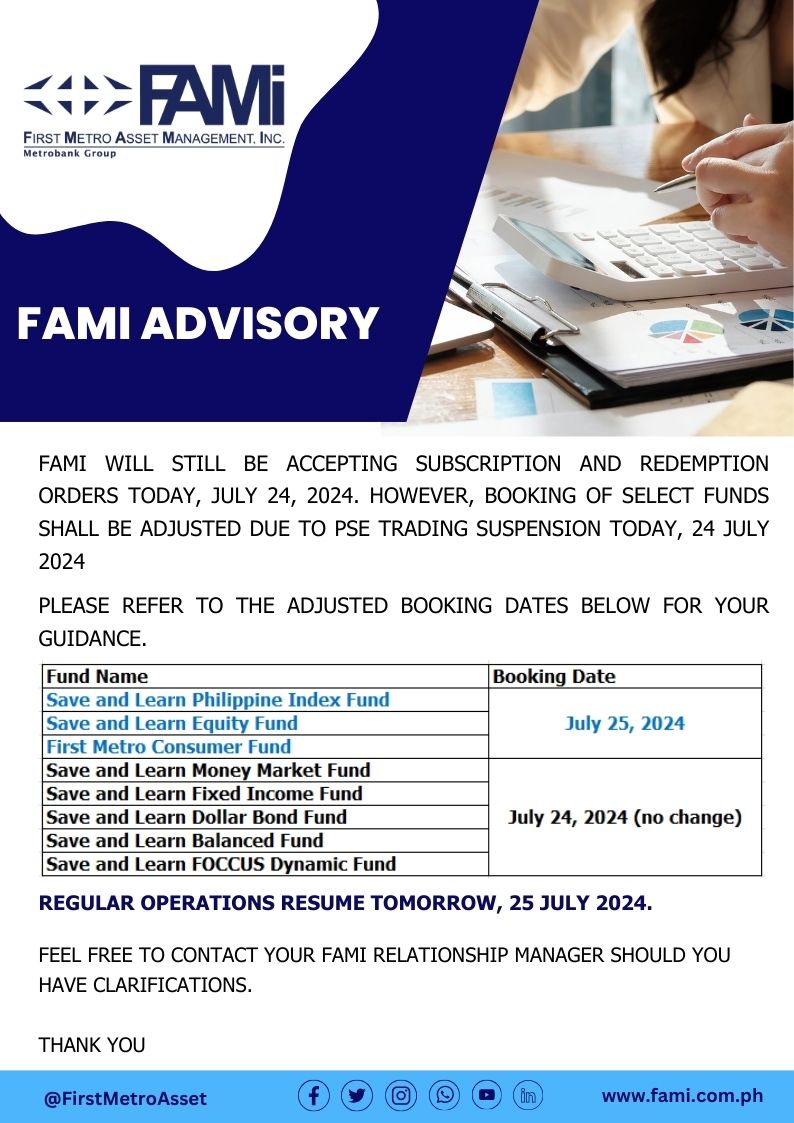

8:48 am Monday 8 August 2011

The biggest headline item in the news over the weekend was the credit rating downgrade of the U.S. by the agency Standard & Poors. I think if one watched CNN, CNBC, Bloomberg and BBC over the weekend, commentators analyzed this issue to death already. What people expect should no longer come as a surprise to us. Of course there will be a lot of political bickering in Washington D.C. as well as populist and conservative economic and political analyst painting their own doomsday scenario.

My take on the events of the past week is that the huge declines in the U.S. stock market following the S&P announcement looks like investors had already been anticipating such a downgrade already. I think that the downgrade was more of S&P asserting its credibility rather than an urgency in trumpeting to the world that the U.S. is in credit trouble. Everybody was watching that particular event as in went to the wire in the U.S. congress when they came to a deficit reduction agreement on Monday last week.

Analysts who pounded the downgrade issue to death foresee a rise in borrowing costs for businesses and consumers alike. I do not know if that is going to happen, but in my experience, borrowing costs of U.S. businesses were determined by the cost of money in the open market. In the short end, that cost is determined by the Fed Funds rate and free markets such as the commercial paper market and other money market pricing mechanisms such as LIBOR. I do not see free skyrocketing anytime soon because Fed Funds will not raise interest rates at all. We may see some steepening of the U.S. government yield curve as people may be unwilling to take larger positions on long maturity U.S. debt, but I think long yields have always been market determined. At the end of the day, I think it is much ado over nothing.

In as far as the Philippines is concerned, prior to this down grade, our credit rating disparity from the U.S. was the notched between AAA and BB which is our current S&P rating. On quick look, that tells me that the notched have decreased by one, meaning our credit rating has moved closer to that of the U.S. How can that be bad for us? Actually, if one looks at how the credit spread on Philippine sovereign bonds have developed over the past few years, you can see that we have improved significantly while other first world countries have declined notoriously.

What is the point of all this anyway? Well, I think putting the credit downgrade in perspective, it merely confirms what a few global economists have been saying since the global financial crisis in 2008 after the Lehman Brothers failure. The economic center of the world which used to be in the U.S. and Europe, generally the Atlantic, has moved to Asia and the Pacific. Fortunately, the Philippines is within the circle of this new center. This was one of the reasons why our currency has been so strong aside from the fact that our foreign exchange cash flows have increased dramatically.

Going down to the stock market, I personally feel that there is very little reason to panic although as I write there is apparent panic in the Japanese market with the Nikkei down 1.35%. The Australian and New Zealand markets are down over 2% while the KOSPI in Seoul is down only0.58%. U.S. stock index futures are down close to 2%. I think the safe haven would be in mining shares particularly because gold prices will tend to be strong. I would avoid property stocks for the time being. I would be neutral on power and energy stocks. I would be a buyer on weakness of banks.

What is important at this point is not to think that you can be a hero. The best thing to do is to watch how prices develop and have the market tell us what to do rather than moving ahead of the market.