Angelo Silva

Oct 29, 2013

2 mins

Near term, I believe that selective stocks in the market have more room to rise due to improved earnings and a favorable macroeconomic backdrop. Investors cannot ignore the stepped up infrastructure spending by government which is spreading spending power throughout the countryside. While the urban centers are seeing improved employment conditions due to the sustained growth of the BPO industry, the prospects for manufacturing and industry are showing more than favorable signs such as new industrial estates being developed to accommodate entrants to the domestic manufacturing space. Rural Philippines continue to benefit from the steady albeit slower growth of OFW remittance as well as the construction of roads, bridges and port facilities. This is quite visible in parts of northern Luzon and the south of Mindanao.

I think this will lead to more capital being attracted to stocks with steady earnings like consumer, property, banks and utilities. While anxiety on the future rise of interest rates continue to haunt us, I think any rises in long term yields will be within the mid single digit level. This should be quite manageable for companies listed in the stock exchange. While a spike in long term yields will undoubtedly affect stock analysts view on stock valuation, I think that growth prospects in the Philippines can outweigh old notions of value as global investors increase their asset allocation into the country.

All told, I think an index level of 6,800 is easily achievable. In fact, I think that a number of non-index stock can outperform the general market as measured by the various indices.

Near term, I believe that selective stocks in the market have more room to rise due to improved earnings and a favorable macroeconomic backdrop. Investors cannot ignore the stepped up infrastructure spending by government which is spreading spending power throughout the countryside. While the urban centers are seeing improved employment conditions due to the sustained growth of the BPO industry, the prospects for manufacturing and industry are showing more than favorable signs such as new industrial estates being developed to accommodate entrants to the domestic manufacturing space. Rural Philippines continue to benefit from the steady albeit slower growth of OFW remittance as well as the construction of roads, bridges and port facilities. This is quite visible in parts of northern Luzon and the south of Mindanao.

I think this will lead to more capital being attracted to stocks with steady earnings like consumer, property, banks and utilities. While anxiety on the future rise of interest rates continue to haunt us, I think any rises in long term yields will be within the mid single digit level. This should be quite manageable for companies listed in the stock exchange. While a spike in long term yields will undoubtedly affect stock analysts view on stock valuation, I think that growth prospects in the Philippines can outweigh old notions of value as global investors increase their asset allocation into the country.

All told, I think an index level of 6,800 is easily achievable. In fact, I think that a number of non-index stock can outperform the general market as measured by the various indices.

Related Articles

Insights and Announcements

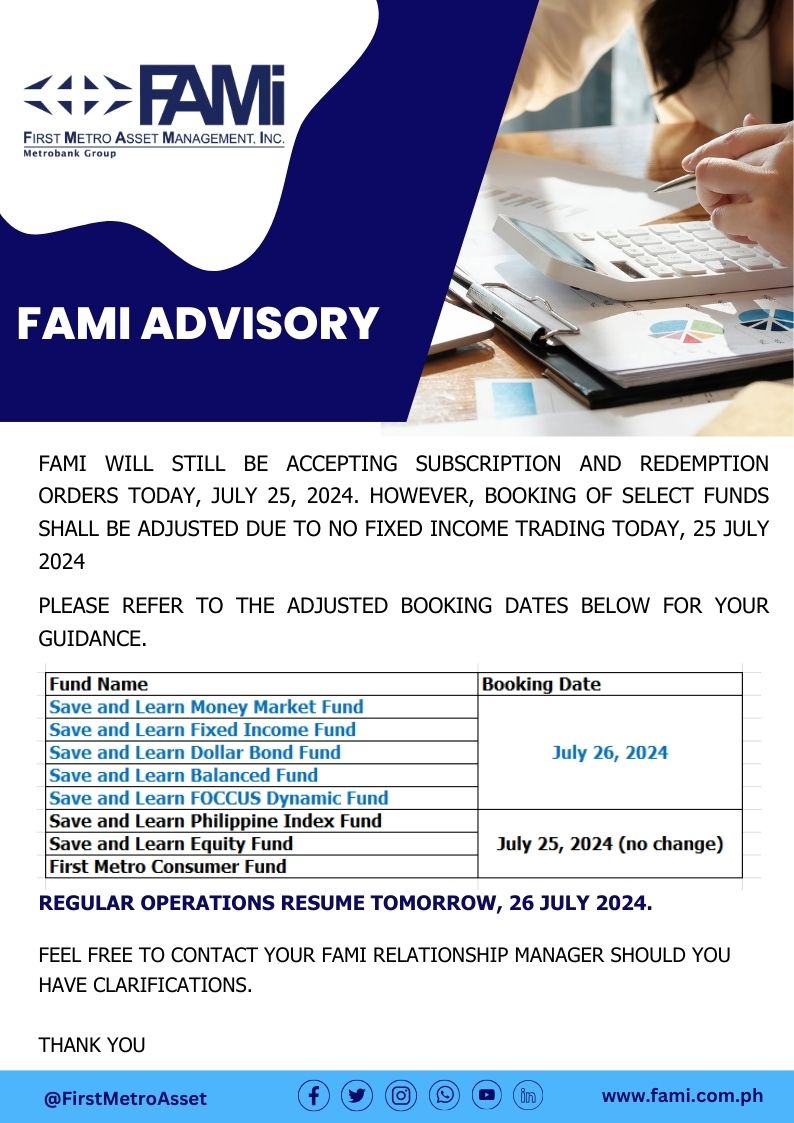

FAMI BOOKING ADVISORY