Written By

Angelo Silva

Angelo Silva

Published on

Feb 19, 2010

Feb 19, 2010

Reading time

4 mins

4 mins

Share this article

Related Articles

Insights and Announcements

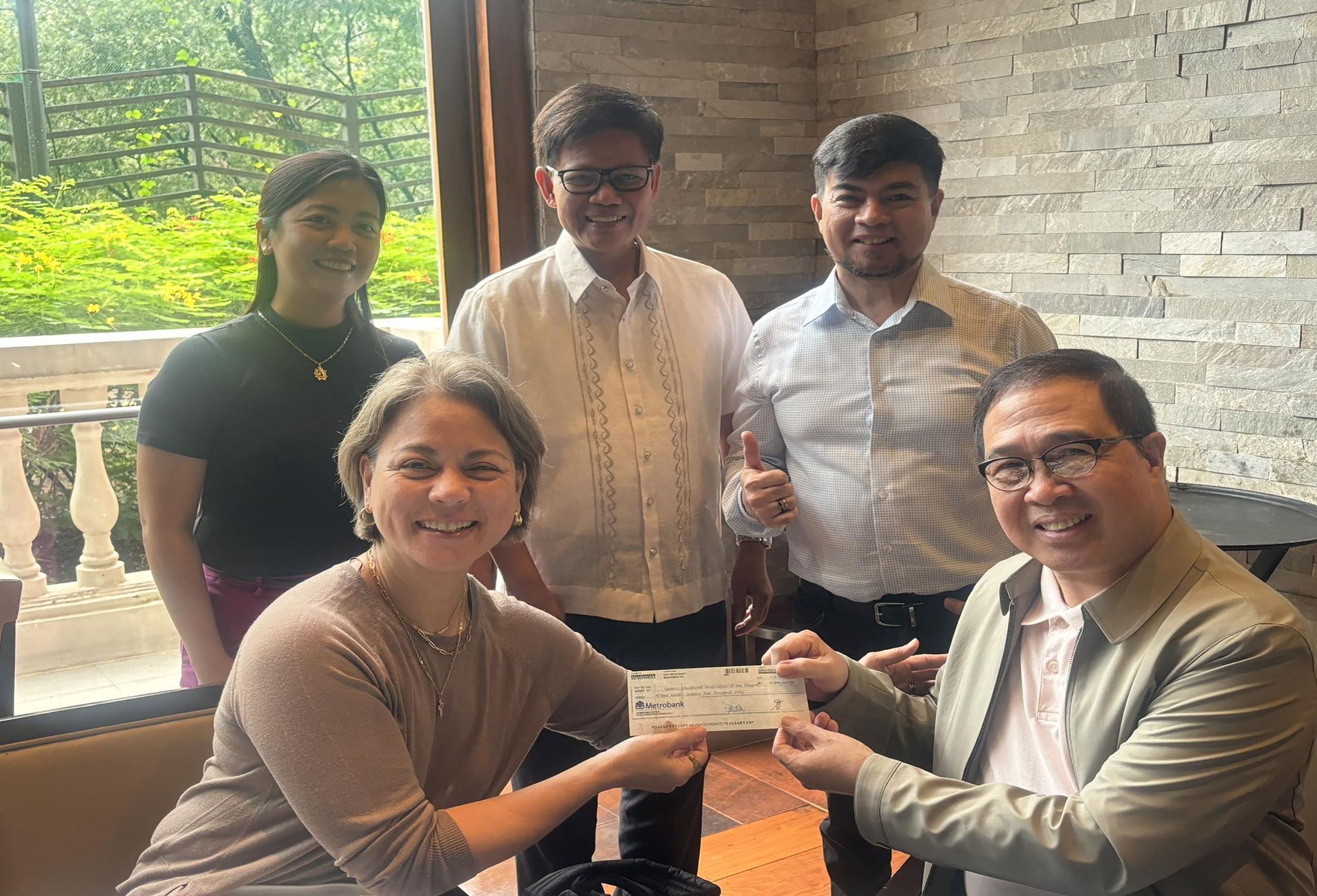

FAMI Releases Php 15 Million in Dividends to Partner Institution CEAP